Personal injury Trust Investment

A personal injury trust investment is an important way for you to protect your compensation award after a claim is successful. The main benefit is to be able to shelter your compensation award from any means-tested state benefits claims.

You should consider a personal injury trust investment if you, or a member of your family, is likely to receive a sizeable personal injury compensation award. This could be as the result of an injury, or medical negligence, and could be paid from a personal injury legal claim, via insurance, or a charitable gift. At the end of the claim process, you may receive a significant amount of money to help you to deal with your ongoing medical conditions, and loss of earnings. This can be a long and arduous process, and your specialist personal injury solicitor will help you through this. When you get to the settlement stage , your solicitor is likely to recommend a personal injury trust investment, since this is a legal way for you to hold your compensation while still remaining entitled to receive means tested state benefits.

Who should read this article?

This article is aimed at people who have suffered a serious illness or injury, and who are likely to claim significant compensation. We explain why a personal injury trust investment is valuable, the impact of using trusts, and also why you might consider not using a trust. We also explain how you can manage your personal injury trust investments once the trust fund has been established.

1. What is a personal injury trust fund?

Personal injury trust funds allow you to receive your compensation without this award affecting your means-tested state benefits. If you claim means-tested state benefits your personal money is taken into account as part of your claim. The size of your personal injury claim often means that if you receive your compensation directly to your bank account you are likely to lose your means-tested state benefits. If your compensation award is likely to be greater than the amount of capital permitted under state benefit rules, you can use a personal injury trust fund to legally shelter this money, and still legitimately claim means-tested state benefits.

Personal injury trusts are sometimes known as “special needs trusts”.

You are due to receive compensation from your claim – what next?

If you have been through a claim for a personal injury or medical negligence, you know the process takes a long time. Now that you are approaching the point where you are due to receive an award, you should take care to plan for the next step. The decisions you make now will have important implications in the future.

Your approach might depend on a number of factors, such as:

The amount of compensation

Your decisions will be different if you expect to receive a large amount of compensation, compared to a smaller lump sum. For example, an award for £20,000 has a different set of decisions than £1 million. We typically work with larger compensation awards (at least £200,000), mostly because they have more complex needs for support. A smaller award might not need a personal injury trust, partly because the practical hassle of using trusts might be worse than the benefits.

Your health

The impact of your personal injury could have profound implications for how you expect to live the rest of your life. It is likely that the reason you were able to claim an award is that you have been severely affected by the injury or negligence. Therefore, you need to plan carefully for how the personal injury compensation will help you to cope with your new reality.

Any personal injury trust investment should be set up to help you deal with these issues, and so must be flexible to cope with your changing expectations in the future.

Your age

The younger your age, the longer you are likely to need to manage the possible personal injury trust investment. Most people who consider this approach are concerned about one thing: will I have enough money in the future? When we recommend a personal injury investment, we aim to assess your financial security and the long-term sustainability of the capital.

Other income and capital

Your other assets and sources of income will have a bearing on whether you choose to set up a personal injury trust. The primary aim of a personal injury trust is to avoid any impact on means-tested state benefits. If you have other income and capital, you might not get as much out of the trust arrangement.

How will my personal injury claim affect my means-tested state benefits?

Many state benefits are means-tested. This means that the state will assess you to establish whether you have a need for the claim you are making based on your other resources. If you have existing income or capital which will continue after the claim, this is likely to affect the amount of state benefits you can be paid. Broadly, the more income or capital you have, the lower your means-tested benefits will be. If you have too much capital, then you will not be entitled to claim means-tested state benefits at all.

Many state benefits are means-tested. This means that the state will assess you to establish whether you have a need for the claim you are making based on your other resources. If you have existing income or capital which will continue after the claim, this is likely to affect the amount of state benefits you can be paid. Broadly, the more income or capital you have, the lower your means-tested benefits will be. If you have too much capital, then you will not be entitled to claim means-tested state benefits at all.

After you receive your personal injury claim you would expect to receive a significant lump sum of capital, and this capital is likely generate at least some income. This compensation capital and income that would probably mean you reduce or lose your means-tested state benefits. A personal injury trust can help you to avoid this issue.

Which UK state benefits are means-tested?

- Income support

- Universal credit

- Pension credit

- Housing benefit

- Council tax support

- Cold weather payment

How much compensation can you hold before means-tested state benefits are affected?

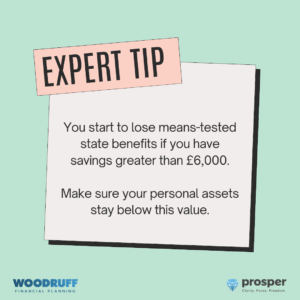

- Less than £6,000 in assets

Your means-tested state benefits will not be affected; - Between £6,000 and £16,000 in assets

Your means-tested state benefits will reduce on a sliding scale until your assets fall below £6,000; - Over £16,000

You are unlikely to be able to claim means-tested state benefits.

If you use a personal injury trust to shelter your compensation claim you can legitimately ignore the injury award when making your means-tested state benefits claim.

52-week grace period

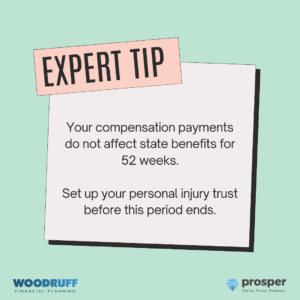

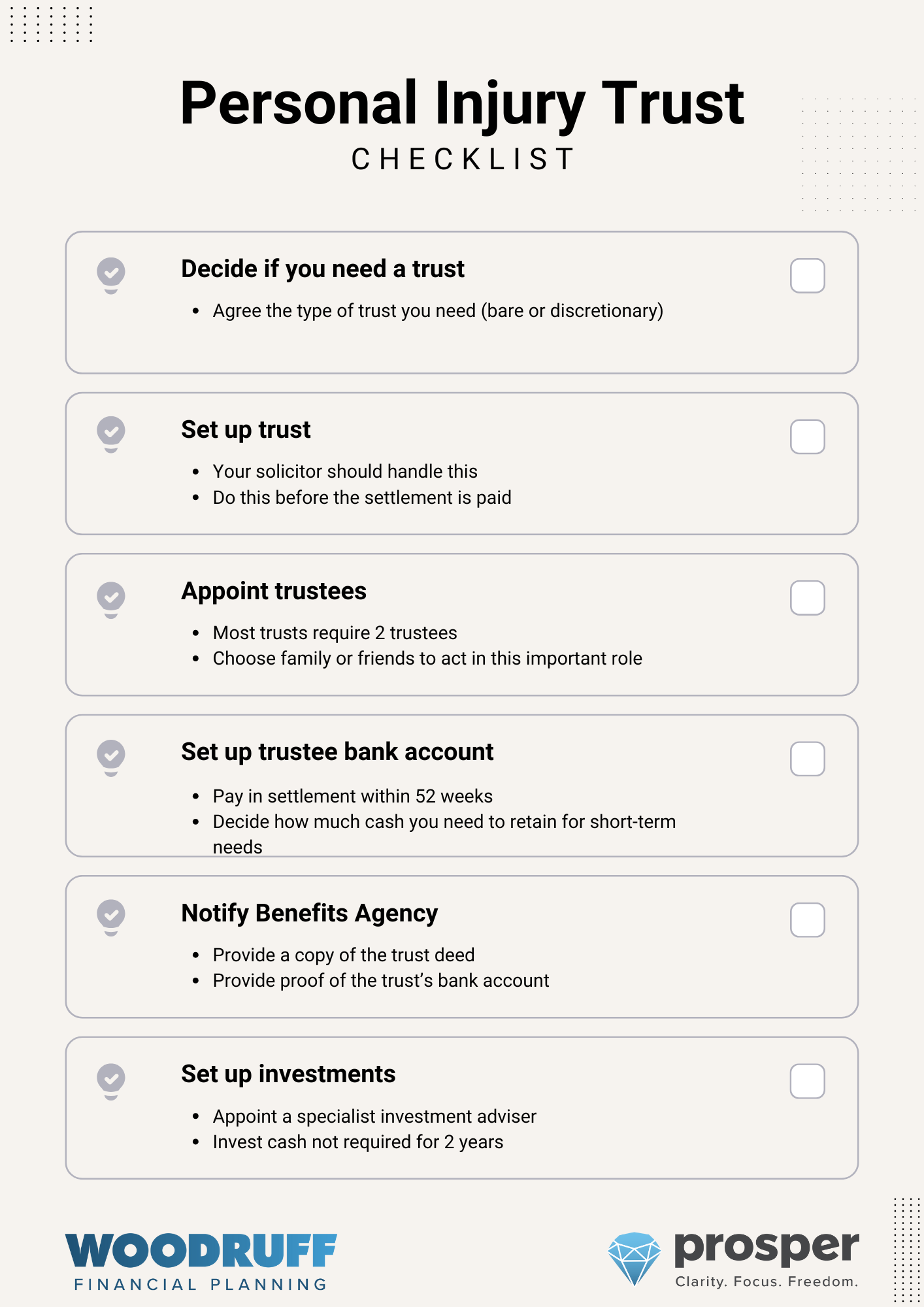

The first payment that you receive after a personal injury will not be counted for 52 weeks after the award, when calculating any means-tested state benefits. This only applies to the first payment, so any future compensation awards may affect your benefits. Therefore, it makes sense to set up your personal injury trust within the 52-week period. Usually, your solicitor will arrange for the trust to be set up before you receive any compensation award. If you set up the personal injury trust after receipt of the compensation, the capital and income may be counted as part of your assessment for means-tested benefits. This will certainly be the case if the personal injury trust is set up after 52 weeks.

The first payment that you receive after a personal injury will not be counted for 52 weeks after the award, when calculating any means-tested state benefits. This only applies to the first payment, so any future compensation awards may affect your benefits. Therefore, it makes sense to set up your personal injury trust within the 52-week period. Usually, your solicitor will arrange for the trust to be set up before you receive any compensation award. If you set up the personal injury trust after receipt of the compensation, the capital and income may be counted as part of your assessment for means-tested benefits. This will certainly be the case if the personal injury trust is set up after 52 weeks.

Do you need to inform the Benefits Agency that you have a personal injury trust?

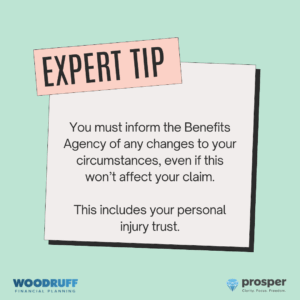

You have a duty to disclose any changes to your financial circumstances, including the receipt of compensation and the establishment of a personal injury trust. You should inform the Benefits Agency as soon as you set up your personal injury trust. It is common for your personal injury solicitor to handle this part of the process for you.

You have a duty to disclose any changes to your financial circumstances, including the receipt of compensation and the establishment of a personal injury trust. You should inform the Benefits Agency as soon as you set up your personal injury trust. It is common for your personal injury solicitor to handle this part of the process for you.

- Provide a copy of the trust deed

- Provide proof of the trust’s bank account (which should be separate from your own funds)

They should be used to dealing with personal injury trust claimants, and will be aware that your compensation should be ring-fenced from your means-tested state benefits claim. Bear in mind that the Benefits Agency will be looking for any regular income withdrawn from your trust, so you need to ensure that you do not take income out of the personal injury trust that could affect your claim (see the Practical Considerations section below).

Personal injury trusts and care costs

Personal injury trust assets are not counted for local authority care assessments. This is an important issue to consider, even if you do not need care right now. If you set up a Personal injury trust correctly, any future care might be paid by the local authority rather than the trust.

Deprivation of assets

Normally, local authorities have strict rules around “deprivation of assets”. This means that you cannot give away money (such as to a trust) so that you can reduce your assets and therefore qualify for support for care fees. For Personal injury trusts these rules are ignored. This makes these trusts an effective way to avoid care fee costs.

Do I need a personal injury trust if I’m not on state benefits or do not need care?

The short answer is that nobody needs a personal injury trust investment. Most people set them up to avoid affecting their state benefits and to shelter assets against the future costs of care.

State benefits

If you are not on state benefits this is a difficult decision, as you would probably rather retain full control over your compensation award. If this is the case, you may not want to set up a personal injury trust.

However, you should consider whether it is likely, or possible, that you might claim means-tested state benefits in the future. If so, you would be glad that you have sheltered your compensation award from this assessment. You cannot set up a personal injury trust after the award has been paid out.

Care fees

The same considerations apply for care fees. You should consider whether you might need to pay care fees at any stage in the future. If so, having your compensation award in a trust should mean you can shelter assets from this assessment.

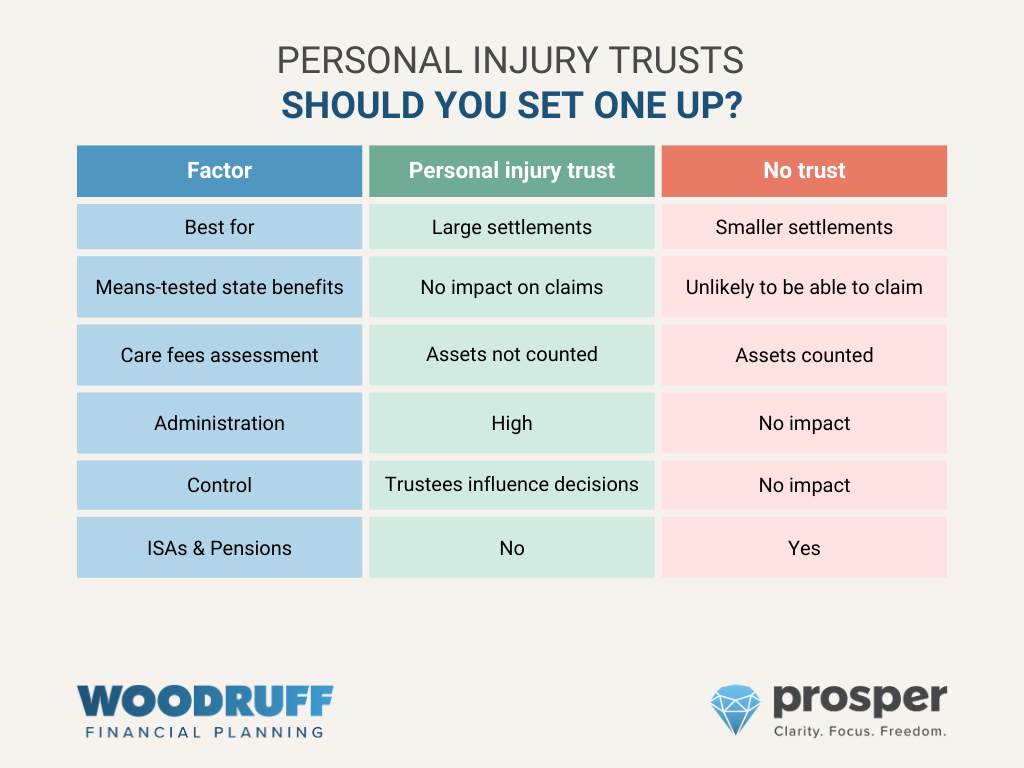

Comparison of a personal injury trust versus receiving compensation directly

See below a summary of the advantages and disadvantages of each option:

What is a trust?

A trust is a legally binding way for you to hold money separately from your own affairs, so that your compensation award does not affect your means-tested state benefits (and those of your close family). The downside of this approach is that you have strict rules to follow if the compensation award is held within a trust.

How does a trust work?

A trust is a separate legal entity from a person, and is able to hold assets, receive income, and pay taxes much like a person or a company. Trusts are subject to complex rules and onerous responsibilities.

A personal injury trust has 3 important roles:

The Settlor

This is the person who sets up the trust. This person would be the one who is receiving the personal injury compensation. The settlor is the person who make the initial payment of the compensation award into the separate legal entity.

The trustees

The trustees are responsible for the management of the trust. They hold the legal ownership of the trust’s assets on behalf of the beneficiary (see below). Trustees have important duties and responsibilities and must look after the beneficiary’s best interests.

The trustees are responsible for the management of the trust. They hold the legal ownership of the trust’s assets on behalf of the beneficiary (see below). Trustees have important duties and responsibilities and must look after the beneficiary’s best interests.

You should choose your trustees carefully, as they will have some control over how and when you are able to access your settlement money. Trustees are in a position of some control and responsibility over the personal injury compensation award money. Therefore, this is not a position to take on lightly, as you may be required to make regular decisions, keep records, manage assets, and pay taxes.

To read more about the role of a trustee see our trustee investment guide.

The beneficiary

This is the person who benefits from the trust assets, and would be the same person as the settlor in the case of a personal injury trust fund.

The trustees manage the personal injury trust on behalf of the beneficiary, who is the person that should benefit from any compensation award.

Who can be trustees for a personal injury trust?

Personal injury trustee need to be aged over 18. Trustees are usually trusted family members, or close friends; alternatively, professional advisers such as solicitors can act as trustees.

Types of personal injury trust fund

Bare trusts

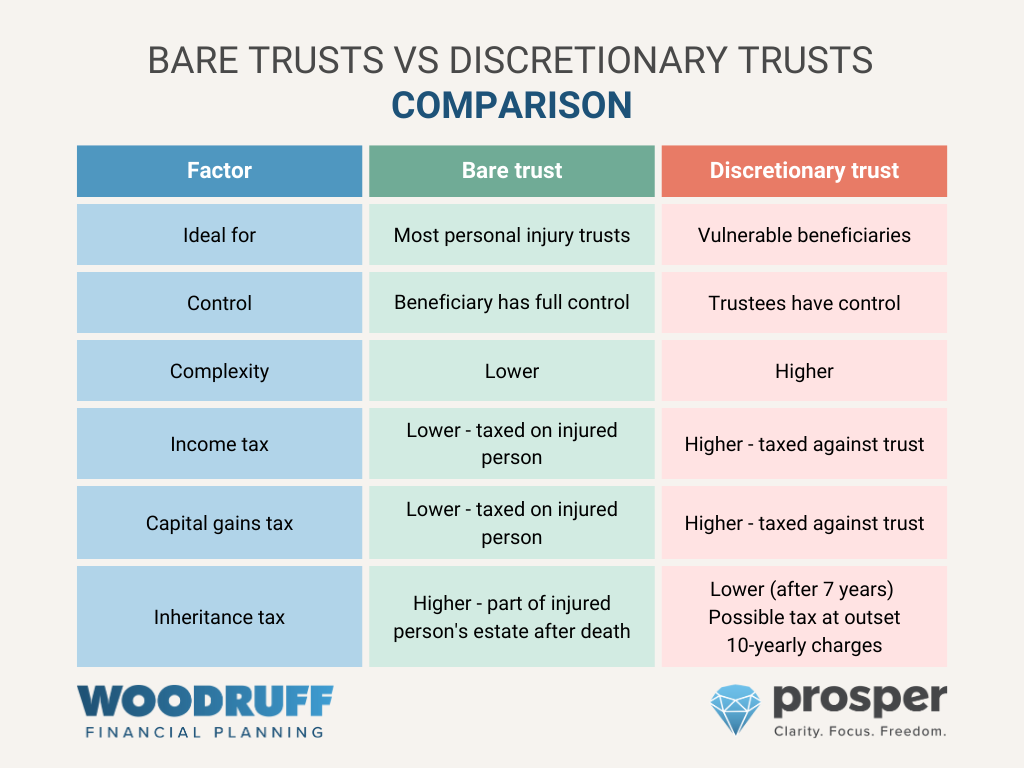

Most personal injury trusts are bare trusts. Bare trusts are usually appropriate for a personal injury trust because they give the injured person the most amount of control.

Most personal injury trusts are bare trusts. Bare trusts are usually appropriate for a personal injury trust because they give the injured person the most amount of control.

Using a bare trust means that the injured person can demand access any or all of the capital held in the trust at any stage. This is important, because this gives the injured person more control. They can decide to take assets out of the trust at any stage. Effectively, this gives the settlor the opportunity to wind up the trust.

Bare trusts are taxed against the injured person (whether or not withdrawals are taken). The tax on individuals is usually better than other types of trust, so this is likely to be the best option. Tax rates start at the usual rates that apply to individuals.

When the injured person dies the trust assets will revert to their estate, and pass according to their will. Therefore, bare trusts do not help to save inheritance tax.

Bare trusts are the most simple trust arrangements, but they still come with a variety of legal complications and potential pitfalls.

Discretionary trusts

You can set up a personal injury trust fund as a discretionary trust. This means that the trustees have discretion over when and how capital or income is paid out of the trust.

You can set up a personal injury trust fund as a discretionary trust. This means that the trustees have discretion over when and how capital or income is paid out of the trust.

Discretionary trusts are less common than bare trusts for personal injury situations, because they are more complicated to run and have generally higher tax. Your solicitor might recommend a discretionary trust to protect a vulnerable beneficiary, such as someone who is unable to make decisions for themself. Examples might be for disabled children or someone with a brain injury, who does not have the capacity to manage their own financial affairs.

Tax in discretionary trusts is paid by the trust rather than the injured person. Discretionary trusts are usually subject to more onerous tax than bare trusts, and get lower tax allowances than individuals. For example, income tax is at the highest rate (39.35% for dividends and 45% for other income). From 6th April 2024, discretionary trusts with total income below £500 face no tax liability and generally have no reporting requirements. Discretionary trusts with income of £500 or more face taxation on the entire amount at the rates quoted above.

Discretionary trusts may be subject to inheritance tax at 20% when they are created if the settlement is greater than £325,000. These trusts may also pay additional tax charges every 10 years (the periodic charge). This charge is calculated on the growth in the discretionary trust assets over £325,000. This may be up to 6% of this growth, payable every 10 years.

After 7 years, discretionary trust assets will be outside of the injured person’s estate for inheritance tax. This means that when they die, the trust assets should not be chargeable for inheritance tax. This is one other advantage of a discretionary trust over a bare trust. Just remember, that the primary aim of the personal injury trust is to look after the needs of the injured person. Therefore, the potential benefits of avoiding inheritance tax are likely to be of secondary importance.

Comparison of bare trusts against discretionary trusts for personal injury cases

Read more about the taxation of different types of trust.

Do I have to set up a personal injury trust fund?

No – the default position is that any compensation payment will be paid directly to your own bank account. If you receive means-tested state benefits then your solicitor is likely to recommend, or at least discuss the benefits of a personal injury trust fund.

You can of course decide that you prefer to take the claim money into your own hands, but you risk losing valuable means-tested state benefits if you take this action.

When might you decide against a personal injury trust?

- If your settlement is relatively small

If you receive a relatively small settlement, perhaps less than £20,000, then the costs and administration of a personal injury trust may not be worthwhile. You may instead choose to receive the settlement directly, and simply spend the money. - If you want full control of your settlement

You may decide that you do not want any outside interference in your financial affairs. If your personal injury settlement is greater than £16,000 you should be prepared to see your means-tested state benefits reduced or stopped.

What if I later need nursing care?

One possible benefit of a personal injury trust is that if you later need to go into a nursing care home, your trust assets will not be taken into account for the financial assessment. This means that the cost of care will not be paid from your compensation fund.

2. Practical considerations for personal injury trusts

Once you have decided to set up a personal injury trust, this is not the end of the matter. You have to continue to manage your personal injury trust properly, to ensure that you get the maximum benefits from the process, and also avoid unwanted pitfalls.

How will the personal injury trust be used?

By placing your compensation money into a personal injury trust, you naturally place certain restrictions around the use of the money. The primary reason for setting up the trust is to shield assets from calculations in means-tested state benefits. This means that you must be careful in how you spend any trust money, or you may risk losing state benefits.

You may need to inform the Benefits Agency that you have a personal injury trust, to avoid any future misunderstandings about your assets.

How do you set up a personal injury trust?

Your solicitor will arrange the trust

In most cases, your personal injury solicitor should arrange for the personal injury trust to be set up once your compensation award is agreed.

From there, the compensation money will be paid into the trust, and you will need to appoint trustees to manage the assets on behalf of the injured person. Trustees are legally responsible for the management of the trust money, and have strict duties to look after the interests of the person who is to benefit from the trust. Read more about trustee responsibilities.

What if your solicitor does not arrange the trust?

Many solicitors specialise in personal injury claims, but do not set up personal injury trusts. This can be frustrating, since your solicitor recommends a personal injury trust, but is not in a position to help you to set this up. We do not do this work, but we have arrangements with personal injury trusts specialist solicitors, who have experience managing trusts and dealing with compensation claims.

If you would like to set up a personal injury trust, contact us, or call 01206 919101.

What funds can be placed into a personal injury trust?

A personal injury trust can accept money from a variety of sources, such as:

- A personal injury legal claim

- Compensation from the Criminal Injuries Compensation Authority (CICA)

- Compensation from the Motor Insurers’ Bureau for injuries caused by an uninsured motorist

- An armed forces compensation scheme award

- Charitable donations

- Payments from accident or travel insurance

- Payments from medical negligence claims

Appointing trustees

If you are responsible for a trust, you are known as a trustee. You will have the legal right to deal with assets according to the terms of the trust, and to your duties as a trustee. Your main role is to look after the interests of the beneficiaries – those who are entitled to receive benefits from the trust.

The choice of trustees is an important one. Most people choose trusted family members or close personal friends. You can also choose a professional trustee, such as your solicitor, but in most cases this is not necessary. Bear in mind that a professional trustee will charge you fees for the service.

Trust bank account

It is extremely important that you keep personal injury trust assets separate from your own money. The reason for this is that the Benefits Agency and local authority might conclude that trust assets are actually your own assets. If so, they might cease state benefits or care fees. If you mix trust assets with your own, you risk seeing reductions in your benefits or care assistance.

It is extremely important that you keep personal injury trust assets separate from your own money. The reason for this is that the Benefits Agency and local authority might conclude that trust assets are actually your own assets. If so, they might cease state benefits or care fees. If you mix trust assets with your own, you risk seeing reductions in your benefits or care assistance.

Personal injury trusts will need a trustee bank account. This trustee bank account will hold some or all of the compensation payment, at least until you are ready to distribute the proceeds or invest them. The trustees will need to set up the account as they are the legal owners of the compensation payment, and you must keep the trust’s money separate to your own finances.

This can be a frustrating process as many banks have complex administration when dealing with trustee accounts. The trustee bank account will be used to receive any cash of the trust, and to make payments such as expenses of the trustees. It is common for trustee bank accounts to require 2 trustees to authorise transactions.

Banks offering personal injury trust accounts

We have found in recent years that many banks have removed trustee banking facilities. This is a specialist area, which most banks do not want to offer.

Here is a list of banks, who we know offer trustee accounts:

- Metro Bank

- Cater Allen Bank

We do not make specific recommendations for these products. Other banks may offer trustee services.

What can I do with the personal injury trust money?

In general, there are no restrictions over how you choose to spend your personal injury trust money. After all, the compensation was awarded to you for your benefit, so you should get to spend it how you wish.

Here is some general guidance for how you should use your personal injury trust.

Keep your own money separate from trust money

It is extremely important that you do not mix these assets as this could mean you lose state benefits.

Use state benefits for regular living expenses

The point of your state benefits is to provide for your general living expenses, so use this money for this purpose.

It is better for you to use your normal income from state benefits for expenses like:

- Food

- Utilities

- Housing

- Council tax

Do not over-use your personal injury accounts

You should ensure that you spend your own money, where appropriate. Partly, you want to avoid accumulating assets that would affect means-tested benefits.

You also should take care not to exhaust your personal injury trust too quickly, so you can sustain your capital for as long as possible.

Personal injury trust income

The income in the trust will usually be taxed on the injured person, but this should not affect your state benefits.

Avoid withdrawing regular income from any investments held by the trust. If you take regular income from the trust, you are likely to create an assumption that this should be counted for means-tested benefits assessments.

Trust assets that generate income need to be declared:

- For bare trusts – this is the responsibility of the injured person

- For discretionary trusts – this is the responsibility of the trustees

Assets that are likely to generate income (in the trust)

- Bank accounts

- Investments – such as shares, general investment accounts

- Rented property

We sometimes recommend assets that do not produce an income for your personal injury trust investments, since this avoids the requirement to declare this in tax affairs.

It is possible for income to be generated by trust investments, but for this not to affect your state benefits, provided withdrawals are not taken from the trust.

Personal injury trust capital

The capital belongs to the personal injury trust until it is distributed to the injured person. While this capital sits in the trust, you do not need to worry about it affecting your state benefits calculations. However, if you withdraw any capital from the trust, this is when you have the potential to cause problems with means-tested state benefits. You should aim to have no more than £6,000 in your personal account at any stage. For this reason, it is better for trustees not to make large distributions to a beneficiary.

Trust withdrawals for one-off items

Withdrawals from the trust should be used to fund specific items of expenditure, and should be for the benefit of the injured person.

Withdrawals from the trust should be used to fund specific items of expenditure, and should be for the benefit of the injured person.

Payments should be for one-off items, not regular expenditure. Trustees should vary dates when payments are made, to avoid the assumption that this is a regular transaction.

This could include any of the following:

- Buying equipment to help with your disability

- Adapting your home

- Medical treatments

- Holidays or leisure

- Vehicles

- Clothing

Trustees can make payments directly to suppliers to avoid money passing through the beneficiary’s bank account. For example, if the trustees were to decide to buy a car for the beneficiary, they could pay the dealership directly from trust funds, to avoid the money passing into the injured person’s account.

Provided that you are an adult with no mental incapacity there should be no reason for trustees to refuse any request for a withdrawal from the trust, unless the trust is a discretionary trust.

Can I add money to the personal injury trust later?

The only money that should be placed into the personal injury trust is the financial settlement from your compensation. If you withdraw any money, you should spend this as intended.

You cannot put this money back into the trust once it has been taken out, and you cannot add to the personal injury trust fund in the future.

Keeping records of the personal injury trust

The personal injury trust is a separate legal entity, and trustees should keep records to ensure that the trusts affairs are separate from the injured person’s affairs. The trustees of the personal injury trust are responsible for this requirement.

Trustee Registration Service for personal injury trusts

Generally, personal injury trusts are exempt from the Trust Registration Service.

Tax returns for personal injury trusts

Trustees may be required to submit tax returns. This is less likely for a bare trust, since the tax on any investments held by the trustees will probably fall on the beneficiary. However, trustees of bare trusts are entitled to submit tax returns in rare cases. This might be necessary where the trustees believe it is in the best interests of the beneficiary for them to handle the tax affairs.

Trustees of discretionary trusts will need to submit a tax return.

Other duties and responsibilities for trustees

There are a host of general rules and duties that trustees of personal injury trusts must follow.

Read more about trustee duties and responsibilities.

What are the costs of managing a personal injury trust?

The costs of managing a personal injury trust do not have to be large, especially if family or friends act as trustees.

- Legal fees

You will incur fees when the personal injury trust is drafted, but often ongoing legal advice is not required unless you appoint a professional trustee. - Accountancy fees

You may incur ongoing accountancy fees, especially if your personal injury trust pays regular tax, and needs to submit trust tax returns. - Financial advice fees

You may incur ongoing fees for management of the personal injury trust investments, if appropriate (see below). These fees can be deducted from any investments owned by the trust, unless the trustees prefer to pay the fees separately.

3. Personal injury claims for a child

Children’s personal injury claims can be daunting if they are not understood properly. There are issues you need to consider when managing a child’s personal injury claim. As a parent you will need to consider your child’s future once the settlement has been paid. There are particular issues you should be aware of when managing assets on behalf of a child.

Personal injury claims for a child

A child’s personal injury claim has particular issues, which make it slightly different to those made by adults. The obvious issue is that the child is too young to manage their own affairs, and so a suitable adult (usually family members, such as parents) will have to take control over their personal and financial affairs.

This is more relevant where your child has a personal injury that limits their mental capacity in some way.

There are 2 main established routes for managing personal injury claims for children, after the settlement has been paid.

- Personal injury trusts for children

This is a separate legal entity, designed to hold the assets of the child’s personal injury settlement. The main reason for using a personal injury trust for children is to separate the child’s settlement from means-tested state benefits calculations, and Local Authority assessments for care. - Deputyship for children

This is a strict legal process for the Court of Protection to oversee the management of the personal and financial affairs of a child, particularly where they lack mental capacity. The child’s deputy will be required to regularly report to the Office of the Public Guardian, which oversees their decisions. This process also allows you to separate the child’s settlement from means-tested state benefits calculations, and Local Authority assessments for care.

Legal framework where personal injury trusts are for children

There is likely to be Court oversight. Courts often hold the funds until a child is aged 18. However, Courts may approve a personal injury trust if it serves the child’s best interests.

Personal injury settlements – issues for your child

Ongoing needs resulting from the personal injury

If you claim for a personal injury on behalf of a child, they may receive a large amount of compensation. This is usually designed to compensate the child for a range of issues such as:

- Lost future income

- Paying for adaptions to your home

- Paying for practical support to make the child’s life better after the injury

In addition, family members may act as carers to support the child, and this could mean that they have to give up work to fulfill this role.

Lifespan of the child

Given your child’s age, you probably need to think about the very long-term when making decisions about how to manage the personal injury settlement proceeds. If your child is likely to live a normal lifespan, this will mean that you need to ensure that their needs are provided for in the short term, and very long term. This may also mean they you need to consider what happens to your child’s affairs if you die before them.

You should also give some thought as to what happens when the child reaches age 18, as you will need to ensure that whichever method you use continues to be effective after this age.

Financial planning and personal injury settlements

Personal injury settlements for children can be particularly large, given the longer-term nature of the needs of the claimant. If you are responsible for the needs of a child in this situation you are probably particularly aware that you need to take care to do the right thing with this settlement.

Financial planning can help you to visualise how your child’s needs may change over time, and to make financial provision for all likely risks. We can work with you to make sensible provision for your child’s future, so that you can be sure of their security no matter what happens. This may involve investing part of the financial settlement to enable the compensation to last as long as possible, and to help provide for your child’s changing needs in the future.

Personal injury trust for a child

A personal injury trust is a legal mechanism for holding money from a settlement, following a serious injury. This allows you to separate the compensation money received after a claim from your child’s personal assets. The trust is usually managed by 2 trustees (usually family members), who are legally responsible for managing the assets in a fair, and appropriate way. The injured child will usually be the beneficiary of the personal injury trust, and will ultimately be entitled to receive the proceeds of the trust. Beneficiaries of personal injury trusts for children will have particular long-term financial needs.

Your solicitor will advise you on the best legal framework for your trust as there are different options to choose when setting up personal injury trusts for children. Of course, the trust needs to be in place before your child receives their compensation award. They will also advise you on whether you need a personal injury trust, because it may be more practical to hold assets in the child’s name.

Personal injury trusts for children need to be approved by the High Court, since trusts cannot be set up by children without this approval. The Court needs to be satisfied that the personal injury trust is suitable for the child’s needs, at least until they reach age 18, and possibly afterwards. This also involves approving the trustees.

Why use a personal injury trust for a child?

Personal injury trusts for children exist to separate the money from the legal settlement from other money due to the child, such as means-tested state benefits. The general principle of personal injury trusts for children is that the compensation money should be used to pay for future care needs, and not to subsidise the state’s obligations. Therefore, used properly, personal injury trusts for children can allow your child to continue to receive means-tested state benefits even after receiving a very large compensation award. These trusts can also mean that your child also continues to receive support from the Local Authority for care in their home.

It is important to note that money paid into personal injury trusts for children is not to be used for general expenses. The award is designed to pay for specific future care needs, and so trustees should be careful how they allow money to be allocated from the trust.

Downsides of a personal injury trust for a child

The personal injury trust can only hold money from the child’s settlement. Therefore, the trustees only have the power to manage these assets, and not other money, such as income from state benefits. Therefore, separate arrangements will need to be made to manage the child’s general finances, if appropriate. Separate records and accounts will need to be kept for these areas.

Trustees have strict legal responsibilities, although not a strict as deputies (see below).

Deputyship for a child

Deputyship for a child is a legal process, which aims to look after the interests of a child who lacks the ability to make their own decisions. An application is made to the Court of Protection, after which a deputy is appointed (often a family member, such as a parent). This person is then responsible for managing the personal and financial affairs of the child. It is much more involved than managing a personal injury trust, because stricter rules apply to the deputy. In particular, the deputy must report at least annually to the Office of the Public Guardian, which appoints a solicitor to oversee the deputy’s decisions on behalf of the child. It is because of this stringent process that deputyship for children is often preferred to personal injury trusts for children.

Click here to read more about Deputyship and investment management.

Why use deputyship for a child?

The main reason to use deputyship for children is because of the legal oversight that exists, to ensure that the child’s needs are taken care of. Unfortunately, this creates a significant burden on the person responsible for the child’s needs.

Deputyship for children allows your child to continue to receive means-tested state benefits even after receiving a very large compensation award. Your child also continues to receive support from the Local Authority for care in their home.

As with personal injury trusts, it is important to note that money overseen by the deputy is not to be used for general expenses. The award is designed to pay for specific future care needs, and so deputies should be careful how they allow money to be allocated from the child’s funds.

Issues to consider when using deputyship for a child

Deputies have strict responsibilities, since your role has an impact on every part of the child’s life. In general, you are expected to take control over a number of areas, with proper care:

- Paying expenses of the child

- Accessing state benefits

- Making decisions regarding healthcare

- Making decisions regarding accommodation

- Submitting your annual report to the Office of the Public Guardian

Duties of a child’s trustee or deputy

Once the personal injury claim has been settled, and your legal formalities are set up, you are then responsible for managing your child’s assets either in the personal injury trust, or via deputyship. This can be a very daunting process, particularly if you are not familiar with managing large sums of money.

We are specialists in managing personal injury claims for children, and have set up our Prosper service for the needs of people like you who are managing another person’s assets.

Understanding your duties

These duties will be different depending on whether you are a trustee or a deputy.

Trustee duties

- To act in the best interests of the child

- To diversify investments

- To ensure that investments are suitable

- To review investments

- To obtain and consider advice

- To keep records

Deputy duties

- To help make decisions for the child (where authorised)

- To act in the child’s best interests

- To apply a high standard of care, involving relatives and professional advisers

- To help the child understand your decisions, where possible

- To keep proper records

Tax issues

If you are managing children’s personal injury claims, the child is likely to need to submit tax returns to declare income tax, capital gains tax, and other taxes depending on the trust chosen.

Getting financial advice when managing children’s personal injury claims

Financial advice is not a requirement, but can make sense, particularly when dealing with large sums of money, or complex needs of the child. You may wish to consider involving a financial adviser in the following situations:

Managing investments or pensions

If you are responsible for managing significant sums of money you may need to involve a professional adviser to help you to ensure that you look after the person’s interests in the best way.

This may involve:

- Proper diversification of the investments

- Generating appropriate levels of income and capital growth, which may need to change as the child gets older

- Understanding how long the assets should last, given the circumstances and needs of the child

- Managing tax

Making the assets last

A financial plan can help you to understand how long the child’s assets will last given cautious assumptions about the future. You can look at how the child’s needs may change over time, and visualise how their money will have an impact on their future security. Working with a financial planner can help you to establish and justify the right decisions.

4. Financial planning and personal injury trusts

If you are considering a personal injury trust investment, then it is likely that you have received a substantial award as a result of your claim. No doubt, the issue underlying the claim will mean that you have unique personal circumstances, and will need to adapt to these changes for the rest of your life. This will come with a personal cost, and also a financial coat. Of course, this is the reason that you have received your compensation award.

We have set out below the typical financial planning issues that we address with people who have received a compensation award.

Our Prosper service aims to deal with all of these questions, and whatever else is of concern to your financial planning after a serious illness or injury. We help you to understand how your financial life after the receipt of your compensation, and examine how you can remain secure no matter what happens.

Will my future be secure?

You have suffered a serious illness or injury, and the compensation award is intended to help you to live a more comfortable life.

You have suffered a serious illness or injury, and the compensation award is intended to help you to live a more comfortable life.

Most people who receive compensation are concerned to understand if their future will be secure. Financial planning helps you to establish whether your future is secure. A financial plan seeks to establish how your income, expenses, assets and liabilities work together. We can take all of the known data about your financial life and project forward using some sensible assumptions about the future.

- How long will you need access to the money?

The younger you are, then the longer the period we need to make the personal injury trust last. - Will you have enough money?

You will be concerned to know if the trust fund will be enough to live the life you want in the future. - How long will the compensation last?

Even if you have been awarded substantial damages, you should try to assess whether you are likely to reduce the capital over time. If so, your financial plan should estimate how long we expect your trust fund to last.

What can I afford to spend?

You will use your state benefits to pay for much of your lifestyle spending. However, your personal injury trust is designed to be accessed occasionally to top up your normal monthly spending. Your financial planning should aim at assessing how much is realistic, in your circumstances.

We would aim to assess:

- How much can you afford to spend from your compensation?

Clearly, the more you spend, the less you will have in later years. Your financial planning will help you to assess a balanced approach to future spending. - Will large scale spending affect your future security?

You may have some initial large scale spending plans, such as buying a new home, or making adaptations to your existing home. This is perfectly sensible, but there are some further considerations (see below). In particular, consider how a reduction in your available trust capital will affect your future ability to access funds to spend on your lifestyle. Any money spent on initial items will reduce the available pot for the future.

Can you use a personal injury trust to buy property?

Your personal injury trust investment can own property (provided that the trust has been set up to allow this at the outset). Any professionally drafted trust will include powers to own property.

Your personal injury trust investment can own property (provided that the trust has been set up to allow this at the outset). Any professionally drafted trust will include powers to own property.

Normally, we would recommend that your personal injury trust is used to own your main residence if you want to use your compensation funds to make this purchase. You should speak to a solicitor to arrange this transaction, as there could be a risk that you mix up personal funds, and money owned by the trust.

- The personal injury trust owns the property

Bear in mind that if you use the proceeds of your personal injury trust fund to buy a property then you will not own the home yourself. The trust will be the legal owner, which can mean that you have to get permission from the trustees to make alterations, or sell the property in the future. - What if I want to move house?

If you later want to move house you will have to get permission from the trustees. The trust would sell the house, and buy any new property. - Can the personal injury trust own rental property?

It is possible for a personal injury trust to own any type of property, including rental property. However, take care if you plan to hold rental property in a personal injury trust. This is because a rental property would of course pay an income. That income could be taken into account for your means-tested state benefits, if you take withdrawals from the personal injury trust. Therefore, the benefit of the rental property – the income – could unfortunately mean you lose income from your personal state benefits. If you operate a discretionary trust, your personal state benefits would not be affected, but the trust’s income would be taxed at the highest rates (45%).

How are personal injury trusts taxed?

The taxation of your personal injury trust investment depends on the status of the arrangements.

The taxation of your personal injury trust investment depends on the status of the arrangements.

- Bare trusts

If you operate a bare trust the income and capital will be taxed against the injured person. You will be able to use all the usual personal allowances. - Discretionary trusts

If you operate a discretionary trust the income and capital will be taxed against the trust, at the highest rates, with minimal allowances against tax.

Read more about the taxation of trusts.

Legal requirements for the personal injury trust

Registering the personal injury trust

Registering the personal injury trust

If you operate a trust that is responsible for payment of tax, you do not need to register this arrangement. There is an exception for personal injury trusts.- Trust tax return

If the personal injury trust is liable to tax then you are likely to be required to complete a trust tax return to declare any tax due. This is likely to apply to discretionary trusts, or bare trusts where the trustees take responsibility for the tax.

How will my personal injury trust affect state benefits?

The main purpose of the personal injury trust is to avoid any impact on your means-tested state benefits. Therefore, it is unlikely that your benefits claims will be affected, unless you fall foul of the following:

- Income from your personal injury trust

If you generate an income from your personal injury trust then this could be used in your state benefits assessment, and your benefits may be reduced if you withdraw the income from the trust. For this reason, your personal injury trust should avoid withdrawals of income. - Capital withdrawals from your personal injury trust

You should use your personal injury trust to take capital withdrawals to spend on your lifestyle, and large projects to help with your condition. However, be careful to spend the withdrawals, rather than to retain these amounts for the future. If you keep too much money in your own name you may see your state benefits reduced.

Your financial planning should take account of both these areas, to manage the practicalities of your lifestyle spending.

What happens to the personal injury trust when I die?

What happens to the personal injury trust when the injured person dies, depends on the legal status of the trust at death:

- Bare trust

The personal injury trust will form part of the deceased’s estate for tax purposes, and will be distributed according to their will. - Discretionary trust

The personal injury trust will not form part of the deceased’s estate (unless the death was within 7 years of the setup of the trust). The trust can continue after the death of the injured person, according to the general provisions of the trust; alternatively, the trust could be wound up.

How does the personal injury affect the wider family

You should consider the financial planning implications of the wider effects of the changes in circumstances forced on your through the personal injury.

For example, the injured person may need specialist care, that might be provided by a spouse or family member. This may cost you money, or may require that additional person to give up, or reduce work. All these issues could have knock-on effects for your family income. The carer may also be entitled to claim state benefits in their own right.

5. Personal injury trust investments

If you have more than £200,000 awarded to you, you may wish to consider a personal injury trust investment to ensure that you can maximise the capital growth from your compensation. If you leave the award in a bank account then this will lose money compared to the cost of living each year. Also, a bank account is not likely to help your funds grow you want to help the money to provide for your needs for as long as possible it makes sense to consider a trustee investment.

This is a complex area, and the trustees typically need financial advice. Our Prosper service is designed to help trustees with the following personal injury trust investment concerns.

You can read more in our trustee investment guide.

What investment rules do personal injury trusts follow?

Personal injury trust investments are subject to strict rules. Read more about trustee investments.

Personal injury trust investments are subject to strict rules. Read more about trustee investments.

- Trust deed

Your personal injury trust deed will stipulate the types of investments that you can use. - General trustee investment duties

Trustees are subject to strict rules around investing money in trusts.- Duty of care of trustees

Trustees who managed personal injury investments should take their responsibilities seriously, as you may be managing large funds for many years. In general, trustees should exercise reasonable care and shill when managing investments. - Duty to diversify personal injury trust investments

The duty to diversify investments is extremely important when managing personal injury trusts. Most of these trusts can last for decades, and you should expect that investments will have varying performance over the long term. It is vital to properly diversify your trustee investments, and this can easily be achieved by using a financial planner like us. Diversification means using appropriate assets for the term and risk profile of your trust, and to invest into different types of investments. It is unlikely that simply putting the trust money in a bank account will be appropriate. - Duty to review personal injury trust investments

You cannot simply invest the trust fund and then forget about it. You have a duty to regularly review the progress of investments over time, especially given that a personal injury trust investment could last for decades. - Duty to obtain and consider investment advice

You should consider advice from a variety of appropriate experts. This may include any, or all, of the following:- Investment advice

From a financial planner - Tax advice

From an accountant or tax adviser - Legal advice

From a solicitor

- Investment advice

- Duty of care of trustees

For more information see our article on trustee investments.

How to choose the right personal injury trust investment?

Personal injury trusts can invest in a variety of different investment types. It is important to select the correct investment tax wrapper given the trust’s legal structure (bare trust or discretionary trust), the need for capital withdrawals, and the term of the trust.

Personal injury trusts can invest in a variety of different investment types. It is important to select the correct investment tax wrapper given the trust’s legal structure (bare trust or discretionary trust), the need for capital withdrawals, and the term of the trust.

- Getting the right tax structure

We help trustees to understand the best investment wrapper according to the needs of the trust and the beneficiary. Our default position is to use a general investment account for most bare trusts. The reason is that the tax on these accounts goes against the beneficiary which is usually lower over time. For some personal injury trust cases we recommend investment bonds, since these allow us to avoid income on the trustee investments, while generating tax-efficient capital growth over time. This can be an important factor when sheltering money from state benefits calculations. The decision over the type of investment account depends on a variety of factors. - How often will you need to access the personal injury trust?

In general, the capital from a personal injury trust investment should be accessible for capital withdrawals on an occasional basis. Therefore, providing access to your investments is sensible. Of course, it is possible to invest in any type of asset, such as property, but consider how your beneficiary will access the capital for withdrawals if required. - What is the term of the personal injury trust?

Generally, most personal injury trust investments are long-term in nature, given that they are intended to last for the whole of the injured person’s lifetime. Therefore, it is usually inappropriate to invest in bank accounts, since these are likely to provide low returns when compared to inflation. If you want your personal injury trust investments to last as long as possible then you may want to consider taking some investment risks.

Our prosper service is designed to help trustees to make the right decisions with their investments.

How to manage personal injury trust investment risks

Many personal injury trustees are family members with little experience of managing large sums of money. If this is the case, you may be too cautious when taking investment decisions on behalf of the injured person. Our role is to help you to structure trustee investments using a professional approach, within stated levels of risks. The point of this is to help you to manage the investment appropriately, but more importantly to take sensible decisions to help the compensation last as long as possible.

Keeping enough cash for personal injury trust investments

Keeping enough cash is an important way for your personal injury trust to cope with short-term spending plans, as well as dealing with longer-term volatility in your investments.

Keeping enough cash is an important way for your personal injury trust to cope with short-term spending plans, as well as dealing with longer-term volatility in your investments.

This is a vital part of the advice we give to trustees. We assess how much is appropriate to reserve in cash so that you can cover your planned and unplanned spending, no matter what happens.

This generally falls into 3 categories for personal injury trustees:

- Emergencies – a sensible amount set aside just in case a short-term crisis happens (such as an unexpected expense, or short-term care costs)

- Projects – known larger expenses, such as the purchase of equipment, medial bills or a new car

- Known expenses – we generally recommend that trustees set aside planned spending for the next 2 years. This could be for semi-regular expenses like medical bills, holidays etc.

How to maximise investment returns

You will want the trust’s money to last as long as possible, so we aim to help your funds grow over time. We also try to allow for the flexibility required to take withdrawals as necessary, to help fund the injured person’s needs. Read more about our investment philosophy.

Can a personal injury trust invest into an ISA?

Unfortunately, it is not possible to use a personal injury trust to take advantage of the tax-free benefits of an ISA. This is because ISAs can only be owned by individuals, and not trusts. This means that any investments owned by your personal injury trust will be taxable.

The personal injury trust investments can minimise tax, since they can take advantage of tax-free allowances that exist for the beneficiary of the trust. This can be a complex area, and we can advise you on your options.

Can I take withdrawals from my personal injury trust investment

Yes, you can take lump sum or regular withdrawals from your personal injury trust investments, depending on the terms of the scheme chosen. In practical terms, it may make sense for you to only take withdrawals when you plan to spend the money, since you would not want to build too much cash in your personal bank account. In some personal injury trusts the withdrawals are made directly to suppliers to avoid the money passing into the injured person’s accounts.

6. Free illness and injury mini guide

You can download a free illness and injury mini guide. This covers many tips useful to readers of this article on personal injury trusts.

Take a look at our articles on Illness and personal injury, managing another person’s assets, and our Prosper service. If you have any questions on personal injury trusts, please contact us.

Personal injury trust checklist

Use this handy checklist to work through important action points for your personal injury trust investment plan.

How long will your personal injury compensation last?

Your settlement could last for the rest of your life with careful planning

This FREE Mini Guide will show you how a personal injury trust with sensible investments can provide long-term security after your claim: pay for your lifestyle expenses, make the money last and shelter your settlement from future claims.

Want to make your settlement last?

Fill out the form below

ILLNESS OR INJURY?

Find out how we help you Prosper after an illness or injury.

MANAGING ANOTHER PERSON'S ASSETS?

Find out how we help you manage another person's assets using our Prosper service.

Do you require a simple system to achieve clarity in your finances?

Focus on the 7 most important figures necessary to create your own basic financial plan.

Discover a straightforward way to eliminate the clutter in your financial life to gain clarity on what is actually important with your money.

Author name: Dan Woodruff FCSI CFP

Certified Financial Planner & Chartered Wealth Manager at Woodruff Financial Planning

Dan Woodruff is a Fellow of the Chartered Institute of Securities and Investment (CISI) and winner of the David Norton Award from the CISI. He is a Certified Financial Planner and Chartered Wealth Manager. He is the author of the financial planning book, the 7 Figures Plan. He is a regular contributor to financial contributions and appears on BBC Essex to discuss money matters. He founded Woodruff Financial Planning to provide independent, specialist advice to business owners and high income professionals in Essex and beyond. See his profile page.