7 Strategies to Avoid Inheritance Tax

This article explores all you need to know about how to avoid inheritance tax in the UK (IHT). We explain who pays inheritance tax, how much inheritance tax might be due, and all the issues you need to know if you want to avoid inheritance tax legally.

Key topics covered in this article

Inheritance tax overview

Inheritance tax is payable in the UK on death, and sometimes when you give away certain assets during your lifetime. Inheritance tax is paid on your worldwide assets (subject to certain double taxation treaties) if you are UK domiciled (a tax status related to residency); if you are domiciled outside of the UK, inheritance tax is usually paid only on UK assets (as the country you live in will have its own rules).

After you die, your representatives will need to calculate the value of all of your assets and deduct any liabilities (debts). The remainder is called your “estate”, and this value is what may be liable to inheritance tax (IHT).

How do you calculate your estate for inheritance tax?

Your estate for inheritance tax purposes is the total of all of your assets worldwide (assuming you are domiciled in the UK). The deceased’s personal representatives (such as Executors of the deceased’s will) need to calculate the total of all their assets valued to the date of death, and deduct any outstanding allowable liabilities. The net position is their estate.

Example estate calculation

John died recently, leaving the following assets:

| Asset | Value |

|---|---|

| House | £500,000 |

| Car | £15,000 |

| Personal belongings | £45,000 |

| Investments | £220,000 |

| Bank accounts | £20,000 |

| Total | £800,000 |

John’s estate is valued at £800,000.

If John also had an outstanding mortgage of £200,000, then this would reduce the value of his estate to £600,000.

Which assets are in your estate?

Generally, anything of value should be included in your estate for inheritance tax purposes. If the asset is jointly owned, then your share falls into your estate. This includes:

- Property

- Bank accounts

- Investments

- Shares

- Business assets

- ISAs

- Antiques

- Jewellery

- Personal chattels

- Vehicles

- Life assurance not held in trust

- Gifts made in the 7 years prior to death

Asset values should be taken at the date of death. You may need to obtain specialist valuations for certain assets.

What is not in your estate?

Your estate may not include certain assets that are deemed to fall outside of your ownership for inheritance tax purposes. Examples might include:

- Pension plans

- Life assurance held in trust

- Other trust funds

Other allowable deductions for your estate

When someone dies all of their outstanding liabilities should be repaid (if possible), using their outstanding assets. Funeral expenses are generally allowable deductions from a person’s estate for inheritance tax purposes.

Other costs incurred after death, such as legal expenses or probate fees related to the estate are not allowable deductions.

UK Inheritance tax and living abroad

The assets that are subject to UK inheritance tax are affected by your domicile. Domicile is your permanent home. This is a complex area, but broadly you are treated as having UK domicile unless you can show that you have domicile somewhere else.

HMRC treats you as domiciled in the UK if you either:

- Lived in the UK for 15 of the last 20 years; or

- Had your permanent home in the the UK at any time in the last 3 years of your life.

If you are domiciled abroad then Inheritance Tax is only paid on your UK assets. Certain assets are excluded:

- Foreign currency accounts

- Overseas pensions

- Holdings in authorised unit trusts and OEICs

If you are domiciled abroad then your estate may be able to reclaim tax through a double taxation treaty with certain countries, if Inheritance Tax is charged twice on the same assets (in the UK and the country where you lived). See here for more information on Inheritance Tax Double Taxation Relief.

What is the UK inheritance tax rate?

Inheritance tax is currently 40% of taxable estates on death.

Estate values can be reduced in many situations, due to tax-free allowances such as the Nil Rate Band and the Residential Nil Rate Band (see below) as well as exemptions and reliefs.

You can reduce the 40% Inheritance Tax rate to 36% if you give at least 10% of your “net estate” to charity.

Certain lifetime gifts are also chargeable at 20%, with a possible further 20% due on death within 7 years of the gift.

The inheritance tax threshold (nil rate band)

The inheritance tax threshold, or Nil Rate Band (NRB), is a tax-free allowance for every person. Currently, this is worth £325,000, and applies to estates on death, or for transfers of assets during your lifetime. This inheritance tax allowance reduces the value of your estate so you avoid inheritance tax on the first £325,000 of your assets. The Nil Rate Band has not risen since 2009 and has now been frozen until 2026, meaning that it is more likely with each year that your estate will be liable to pay inheritance tax.

Example Nil Rate Band in practice

John’s estate is valued at £800,000. He did not make any gifts of assets in the last 7 years. His taxable estate is reduced by the Nil Rate Band (£325,000), leaving a taxable estate of £475,000. John would avoid inheritance tax on the first £325,000 of his assets.

The Nil Rate Band and Married Couples

If a person dies without using their full Nil Rate Band they can pass their remaining Inheritance Tax allowance to their surviving spouse or civil partner. Often, the first person in the couple to die leaves their entire estate to their spouse, which is an exempt transfer for inheritance tax (see below). If this is the case, then their entire Nil Rate Band will also pass to their surviving spouse, and this can be used on the subsequent death of the survivor. In practice, this generally means that a married couple can avoid inheritance tax on up to £650,000 of assets (£325,000 x2).

The amount of Nil Rate Band to pass to the surviving spouse is a percentage of the allowance available, and this will apply to the prevailing Nil Rate Band at the date of death of the second partner. This may be important if the Nil Rate Band was partially used on first death, and changes after the first spouse died.

Example partial Nil Rate Band passing to a surviving spouse

Mary died leaving an estate valued at £1,000,000. £900,000 of this money passed to her surviving spouse, Bill, while £100,000 passed to her son Alan. The transfer to Bill was exempt and can avoid inheritance tax (as it is a transfer between spouses), but the transfer to Alan was not exempt. This means that Mary’s Nil Rate Band was partially used on her death, leaving of the Nil Rate Band £225,000 to pass to Bill.

If Bill were to die a few months later, he would be able to use a new Nil Rate Band of £325,000 (his own), plus £225,000 from Mary, making a total Nil Rate Band of £550,000. If the Nil Rate Band was to increase in the future, then Bill’s own inheritance tax allowance would increase, and the allowance that passes from Mary would increase as a relative percentage of the original allowance. Mary’s Nil Rate Band would pass 69% to Bill.

Previous Nil Rate Bands for Inheritance Tax

Here is a summary of the past inheritance tax thresholds, in case you need it:

| From | To | Inheritance tax Threshold (Nil Rate Band) |

|---|---|---|

| 6 April 2009 | Present (at least to 2028) | £325,000 |

| 6 April 2008 | 5 April 2009 | £312,000 |

| 6 April 2007 | 5 April 2008 | £300,000 |

| 6 April 2006 | 5 April 2007 | £285,000 |

| 6 April 2005 | 5 April 2006 | £275,000 |

| 6 April 2004 | 5 April 2005 | £263,000 |

| 6 April 2003 | 5 April 2004 | £255,000 |

| 6 April 2002 | 5 April 2003 | £250,000 |

| 6 April 2001 | 5 April 2002 | £242,000 |

| 6 April 2000 | 5 April 2001 | £234,000 |

| 6 April 1999 | 5 April 2000 | £231,000 |

| 6 April 1998 | 5 April 1999 | £223,000 |

| 6 April 1997 | 5 April 1998 | £215,000 |

| 6 April 1996 | 5 April 1997 | £200,000 |

| 6 April 1995 | 5 April 1996 | £154,000 |

| 10 March 1992 | 5 April 1995 | £150,000 |

| 6 April 1991 | 9 March 1992 | £140,000 |

| 6 April 1990 | 5 April 1991 | £128,000 |

| 6 April 1989 | 5 April 1990 | £118,000 |

| 15 March 1988 | 5 April 1989 | £110,000 |

| 17 March 1987 | 14 March 1988 | £90,000 |

| 18 March 1986 | 16 March 1987 | £71,000 |

The inheritance tax residential nil rate band

The Residential Nil Rate Band (RNRB) is an extension to the standard Nil Rate Band that applies to your main residence on death. This tax-free allowance allows you to avoid inheritance tax but only if you pass your primary residence to a direct descendant.

Currently, the Residential Nil Rate Band is worth £175,000 per person.

The Residential Nil Rate Band can be transferred to a surviving spouse or civil partner on death, if not used by the first spouse to die. This allows the second spouse to double their Residential Nil Rate Band allowance to £350,000. Combined with the Nil Rate Band, the total inheritance tax allowances are worth £500,000, or £1,000,000 for a married couple.

Criteria to qualify for the Residential Nil Rate Band

The Residential Nil Rate Band does not apply in all cases. You should be careful that your current arrangements do not inadvertently mean you lose one of these important inheritance tax allowances.

Criteria applying to the Residential Nil Rate Band allowance:

- You must have held a “qualifying residential interest” during your lifetime

- This means you owned a property (or share of a property) that was your main residence

- The Residential Nil Rate Band allowance does not apply to non-residential property, such as rental property

- You must pass your primary residence to a direct descendant on death (not during your lifetime)

- Direct descendants include:

- Children, grandchildren, or other lineal descendants

- Children of married partners from previous relationships (step-children)

- Spouses or civil partners of lineal descendants, including widows and widowers

- Adopted children

- Foster Children

- Children subject to special guardianship

- Direct descendants do not include:

- Children of unmarried partners from a (e.g. step-children)

- Parents

- Siblings

- Uncles and aunts

- Cousins, nephews and nieces

- Gifts to discretionary trusts

- Direct descendants include:

- For joint property, your share may qualify for the Residential Nil Rate Band

- if you need to sell or downsize your main residence as you enter nursing care, you can still use the value of the asset sold and qualify for the Residential Nil Rate Band

- The home does not need to be mentioned in the deceased’s will to qualify for the Residential Nil Rate Band

- The allowance is progressively lost if your estate is worth more than £2 million

- If you have a mortgage or equity release on your home, it is the net value after deduction of the loan that qualifies for the allowance

Example Residential Nil Rate Band in practice

Simon recently died leaving behind a house worth £250,000 and investments worth £500,000. His will leaves his estate to his 2 children.

His estate is worth £750,000.

Simon can use his Residential Nil Rate Band against his property, reducing his taxable estate by £150,000 (since the property is worth more than the allowance, and is passed to his direct descendants on his death).

After the application of the Residential Nil Rate Band, Simon’s taxable estate is £600,000.

Combining the Nil Rate Band and the Residential Nil Rate Band

If Simon has not used his standard Nil Rate Band, he may be able to further reduce his taxable estate for inheritance tax by £325,000. Using the same data as above, his taxable estate would reduce from £600,000 to £275,000.

Past and Future Residential Nil Rate Band Allowances

The Residential Nil Rate Band is different according to the date of death:

| Death | Residential Nil Rate Band |

|---|---|

| Before 6th April 2017 | £0 |

| From 6th April 2017 to 5th April 2018 | £100,000 |

| From 6th April 2018 to 5th April 2019 | £125,000 |

| From 6th April 2019 to 5th April 2020 | £150,000 |

| From 6th April 2020 onwards (at least 2028) | £175,000 |

The Residential Nil Rate Band will remain frozen until at least April 2026.

Tapering of the Residential Nil Rate Band

The Residential Nil Rate Band is gradually tapered away for estates worth more than £2 million. The allowance is lost at a rate of £1 for every £2 of assets over the £2 million limit. The current Residential Nil Rate Band will be completely lost if your estate is worth £2.3 million, although this does not affect the standard Nil Rate Band.

The £2 million threshold will rise by the Consumer Prices Index (CPI) but not before from 6th April 2026.

Example tapering of the Residential Nil Rate Band

Nilesh has an estate valued at £2.2 million. His estate is therefore £200,000 above the threshold for the Residential Nil Rate Band. Nilesh’s Residential Nil Rate Band will be reduced by £100,000, from £175,000 to £75,000.

As Nilesh’s estate will not benefit from the full Residential Nil Rate Band, effectively this means that his estate will be subject to £40,000 extra in inheritance tax.

Tapering of the Residential Nil Rate Band and Making Gifts

If you make a gift to avoid inheritance tax (a Potentially Exempt Transfer – see below) you may be able to immediately avoid the tapering of the Residential Nil Rate Band; if this takes effect, the gift may temporarily reduce the Nil Rate Band.

This can be a useful device, as the example below shows:

Nilesh decides to make a gift of £200,000 to his son Vijay. This gift is a Potentially Exempt Transfer, which reduces Nilesh’s Nil Rate Band by £200,000 (£325,000 less £200,000, leaving a remainder of £125,000). This gift will drop out of Nilesh’s estate after 7 years, and his Nil Rate Band will revert to the full amount of £325,000.

The gift will reduce Nilesh’s estate by £200,000, leaving the total value at £2 million. Nilesh will now be entitled to receive the full Residential Nil Rate Band of £150,000, saving £40,000 inheritance tax as a result. After 7 years, the gift will also save a further £80,000 in inheritance tax. If Nilesh were to die before 7 years, then the gift would not be effective for the purposes of the Nil Rate Band, but would have benefited from restoring the Residential Nil Rate Band.

Therefore, it is worth considering gifts, particularly for estates valued just over £2 million.

The Residential Nil Rate Band and nursing care fees

The rules allow you to retain the Residential Nil Rate Band if you are required to sell or downsize your main residence to enter a nursing care home, provided the asset value still passes to direct descendants, and the death occurred after 8th July 2017, and the disposal or downsizing of the home took place after 8th July 2015. This policy reflects the common situation where people who require care need to access the equity held in their home. In this case, the value of the asset sold will be used against the Residential Nil Rate Band, even if this asset is not used to pay for nursing care fees.

Accidental loss of the Residential Nil Rate Band

You may accidentally lose your Residential Nil Rate Band if your estate is not distributed in a way that qualifies for the inheritance tax allowance.

Residential Nil Rate Band and step-children

You should take care regarding the Residential Nil Rate Band where your partner has children from a previous relationship. If you are married, your step-children qualify as direct descendants. If you are not married, then step-children do not qualify as direct descendants.

Example of the Residential Nil Rate Band and step-children:

Gary and Sonia are cohabiting. Sonia has a daughter Mary from an earlier relationship. Gary and Sonia own a house jointly as tenants in common. Their wills leaves their share of the house to Mary. When Sonia dies, her transfer to Mary would qualify for the Residential Nil Rate Band, given that Mary is her daughter. When Gary dies, Mary is not treated as a direct descendant, so this transfer would not qualify for the Residential Nil Rate Band.

If Gary and Sonia marry then the transfer to Mary on Gary’s death would qualify for the Residential Nil Rate Band. The marriage would allow Mary to qualify as a step-child.

Residential Nil Rate Band and trusts

Your Residential Nil Rate Band may be lost if your estate does not pass the residential property to a lineal descendant. The Residential Nil Rate Band is usually available if your property passes as part of your estate, and following the death becomes part of the estate of a qualifying beneficiary.

We have seen older wills set up that pass the value of the main residence to a discretionary trust on death of the first spouse. This used to be a common solution before the Nil Rate Band was allowed to pass to the surviving spouse; this can also be effective to avoid care fees in certain situations. Discretionary trusts often fall foul of this rule since the point of the trust is to pass ownership away from a specific individual. This means that the gift of a residential property to a discretionary trust can fall foul of the Residential Nil Rate Band rules.

The following types of trust should allow you to retain the Residential Nil Rate Band as their aim is to pass the money into the estate of the person receiving the property:

- Immediate post-death interest trusts (IPDI trusts)

- Bereaved Minor’s trusts

- Disabled trusts

- Bare trusts

Even if your discretionary trust can only benefit qualifying family members you are likely to lose the Residential Nil Rate Band, because the discretionary trust would mean that the property does not form part of the family members’ estates.

Therefore, if you have this kind of Nil Rate Band discretionary trust in your will, you may accidentally lose the Residential Nil Rate Band. We recommend that you seek advice on this matter from the legal firm which drafted your will.

When is inheritance tax due?

Inheritance tax is due by the end of the sixth month after the person died. Any inheritance tax due must be paid before your assets are distributed.

How to pay the inheritance tax bill

If you are managing the estate of someone, you will need to obtain a tax payment reference to be able to pay the inheritance tax bill. You can pay the inheritance tax from:

- Your own bank account

This payment can be reclaimed once you obtain Probate (the legal right to distribute the estate) - Accounts owned by the deceased

You need to complete forms to permit this.

Therefore, it is a good idea to think ahead before you die to make sure that sufficient cash assets exist to be able to pay any inheritance tax that is due. Otherwise, your beneficiaries may be in a difficult position that they may need to find the inheritance tax due from other sources, such as loans or their own resources, which could put a strain on their finances. There are some provisions for allowing property to be sold to pay inheritance tax if other assets do not exist, but this could incur interest for late payment of inheritance tax.

Inheritance tax late payment penalties and interest

If you miss the inheritance tax payment deadline the estate will incur interest. These interest rates change periodically according to market rates. You can easily calculate the inheritance tax late payment interest by using HMRC’s inheritance tax interest calculator.

Inheritance tax payments on account

To avoid paying interest on late payments of inheritance tax due you can make payments on account. These are advance, estimated payments. If the final calculation shows that you overpaid inheritance tax, then you will receive a refund of the difference, plus interest. If further inheritance tax was due, this will attract interest as well.

Avoiding inheritance tax for someone else

You may be managing the affairs of another person, perhaps because they are subject to a Lasting Power of Attorney or Deputyship order.

In general, these legal statuses are likely to severely restrict your ability to avoid Inheritance Tax on behalf of the person whose affairs you are managing.

Gifts

You are likely to be able to make gifts on behalf of the person, on occasions such as birthdays or weddings. However, you should also be careful to act in the interests of that person, which generally rules out more substantial gifts that might be effective to reduce Inheritance Tax. If you do want to make substantial gifts you will need to apply to the Court of Protection to do this. Each application will be considered on its own merits. The application is likely to consider whether the gifts affect the future needs of the donor, and whether they previously made such gifts. Gifts are generally only approved where it can be shown that the donor’s interests are not affected.

Business Relief investments

You may be able to conduct Inheritance Tax planning by investing in qualifying shares that attract Business Relief from Inheritance Tax. These are legitimate investments that qualify for 100% reduction in Inheritance Tax once the assets have been held for 2 years. This could be a useful way for you to avoid Inheritance Tax for the person whose affairs you manage. See the section below on Investments for more details.

Inheritance Tax statistics

Here are some interesting Inheritance Tax Statistics for the UK:

- 3.8% of UK deaths (23,000 people) paid Inheritance Tax in 2019/20 (increasing by 0.02% on the previous tax year)

- £6.1 billion in Inheritance Tax was received by HMRC in 2021/22

- £2.8 billion was granted in Agricultural relief and Business relief in 2019/20

- Inheritance tax is expected to represent 0.7% of tax receipts in 2022/23

Source: HMRC.

Inheritance tax and charitable legacies

If you leave a charitable legacy, this can reduce your Inheritance Tax rate from 40% to 36%. To qualify for the reduced charitable Inheritance Tax legacy rate you must give at least 10% of your “net estate” to charity in your will

10% of your net estate

Your net estate is the amount of your assets subject to Inheritance Tax once the Nil Rate Band has been deducted. If you give away 10% of this figure to charity, not only will the charitable legacy avoid Inheritance Tax, but the remaining assets will pay tax at a reduced rate of 36% rather than 40%.

Example

Phillip owns assets worth £425,000. He calculates that if he leaves these assets to his brother Neil, his Inheritance Tax bill would be £40,000 (£425,000 less the Nil Rate Band £325,000, leaves £100,000 taxable at 40%). Neil would get £385,000 on Phillip’s death.

Phillip also wants to support a local charity with a gift of £10,000 on his death. His net estate is £100,000 (£425,000 less the Nil Rate Band of £325,000). Therefore, as the charitable legacy is 10% of the net estate, Phillip’s remaining estate is taxed at 36%.

This leaves Inheritance tax payable of £32,400 (£100,000 less £10,000, leaving £90,000 taxed at 36%).

If Phillip makes the gift to charity, Neil would get £382,600 (£2,400 less than if the charitable legacy was not left).

Of course, if Phillip’s assets grew in value then the charitable legacy would also have to grow to keep to the 10% of the net estate.

7 strategies to avoid inheritance tax

There are many ways that you can legally, and safely avoid inheritance tax in the UK. This section explores the 7 areas you should consider. These are tried-and-tested methods to avoiding inheritance tax, and are completely acceptable to HMRC.

Do you need to take any action?

Before you begin any inheritance tax planning, first ask yourself whether you actually need to make any changes? Begin by calculating your expected inheritance tax – the results may surprise you.

If you do not have an inheritance tax liability, or the expected tax is relatively low, then you may be happy to continue as you are. The main benefit of this is that you get to retain complete control over your assets while you are alive.

Many people take the view that paying inheritance tax is a fair price to pay to retain full control over their assets while they are still alive.

Wills and Inheritance Tax

Making a will is one of the best ways to deal with your inheritance tax planning. This allows you to choose how your assets will be treated on death, so you can do some careful planning and therefore avoid inheritance tax. If you do not make a will, the state will decide how your assets are distributed. This will not be the most efficient way for you to avoid inheritance tax!

Wills and inheritance tax

What is a will?

A will is a legal document, which allows you to deal with how your assets are treated after you die. It also allows you to set out your wishes on other important matters. Ultimately, your will allows you to stipulate who gets what when you die. You can also use a will to avoid tax on your death.

Why should you make a will?

You know that it is inevitable that you are going to die one day. A will allows you to decide how your assets will be treated after you die, as well as other important matters. This can include:

- Who you want to receive your assets when you die?

This will have an important bearing on your inheritance tax planning, especially if you combine your will with other methods of avoiding inheritance tax. - How your dependent children are looked after?

- What happens if those you want to benefit die before you?

- Who is going to manage the paperwork when you die

When someone dies it is obviously a distressing period for their family. Having a will can help to make this time more straightforward than it might be otherwise. Often bereaved relatives find it difficult to make decisions. By having your affairs in order, you can take away a part of the stress of this period.

Intestacy – what happens if you die without a will?

If you die without making a will, the law decides who gets your assets. This is called intestacy, or dying intestate.

In this situation, the law will determine how your assets are distributed after you die. This is unlikely to work as you would have planned, and ultimately means you would lose control over your inheritance tax planning. In some cases, intestacy can spell disaster for your family. If you are married, your spouse will get some of your assets, and the right to an income in some of the rest. Any children would get some of your assets, with some of the surviving spouse’s assets on their subsequent death. If you are not married, your partner gets nothing. This is a complicated area, and the overall message is that dying without a will means unnecessary complications. You should expect that your assets will not be distributed in the way you would have chosen.

The rules of intestacy

The rules of intestacy specify a specific order for dealing with your assets after you die without a valid will. Your family benefits in this order:

- Your spouse or civil partner

- Children and grandchildren

- Parents

- Siblings

- Grandparents

- Uncles and aunts

- The state

If you die without a will then your estate will be divided according to the priority above. Your spouse and children may be considered together (see below). If you have no spouse or children then the priority order will be followed until complete.

If you are unmarried

Your partner will get nothing from your estate, no matter how long you were in a relationship.

If you have a spouse but no children

Your spouse will receive your entire estate.

If you have a spouse and children

Your spouse will receive:

- Your personal possessions

- The “statutory legacy” – the first £322,000 from your estate for deaths after 26th July 2023 (£270,000 previously)

- Half of the remaining assets

Your children will receive:

- The remaining assets divided equally between them.

Children means legitimate, illegitimate and adopted children, but not step-children.

If you have children but no spouse

Your estate is divided equally between your children. Children means legitimate, illegitimate and adopted children, but not step-children.

No spouse or children, but living parents

If you die without a spouse or children, then your estate will be divided equally between your parents.

No spouse, children or parents, but living siblings

If you die without a spouse, children, or parents then your estate will be divided equally between your full siblings (or their descendants if your siblings died before you). If you do not have full siblings (or their descendants) then half siblings get an equal share.

No spouse, children, parents or siblings, but living grandparents

If you die without a spouse, children, parents or siblings then your estate will be divided equally between your grandparents.

No spouse, children, parents, siblings or grandparents, but uncles and aunts

If you die without a spouse, children, parents, siblings or grandparents then your estate will be divided equally between your full aunts and uncles (or their descendants if they died before you). If you have no full aunts or uncles then half aunts or half uncles share your estate equally.

Intestacy and inheritance tax

Clearly, it is unlikely that you would have chosen to set up your estate as defined by the law of intestacy. If you die without a will you lose the ability to control how your assets are distributed, especially if you want to benefit non-married spouses, relations by marriage (such as step-children), friends, or good causes. If you have no living relatives then the state will ultimately benefit.

The main problem with intestacy from an inheritance tax perspective is that the rules often mean that you will pass assets to non-exempt relatives. This can mean that inheritance tax is payable earlier than might have been expected, simply because of a lack of planning.

Examples of intestacy and inheritance tax

Example 1 – spouse and children

Martin recently died leaving behind his wife Tina and their 2 daughters Emily and Zara. Unfortunately, Martin died suddenly, and he never got around to making a will. His estate is valued for inheritance tax at £1,270,000.

Under intestacy rules, Martin’s assets will pass as follows:

- £270,000 passes to Tina outright

- Of the remaining £1,000,000

- £500,000 passes to Tina

- £250,000 passes to Emily

- £250,000 passes to Zara

It is unlikely that this split of assets would have been what Martin would have wanted. In addition, if the family home was owned by Martin solely, and was valued at £1 million, then further complications might arise as Tina would only receive £770,000 worth of assets; potentially, the family home might need to be sold to allow the distribution of assets.

The intestacy inheritance tax calculation works like this:

The £770,000 of assets that pass to Tina are exempt as a spouse transfer.

The £500,000 of assets that pass to Emily and Zara are not exempt transfers. Martin’s Nil Rate Band would be used at £325,000, leaving taxable assets of £175,000, to be taxed at 40%. Martin’s estate would pay inheritance tax of £70,000, which would have to be paid before the assets are distributed.

If Martin had made a will leaving all of his assets to Tina, then no inheritance tax would have been payable.

Example 2 – Unmarried partner and children

Anton recently died, leaving behind his unmarried partner Anya, and their 2 children Camilo and Ernesto. Anton’s estate is valued for inheritance tax at £1,000,000. Of this estate, the family home is valued at £400,000.

Under intestacy rules, Anton’s assets will pass as follows:

- Anya will not receive anything

- £500,000 passes to Camilo

- £500,000 passes to Ernesto

It is unlikely that this split of assets would have been what Anton would have wanted. Effectively, the rules of intestacy would leave Anya without any legacy from Anton, and this might leave her destitute if she does not hold her own assets. In addition, the family home would pass to Anya’s sons.

Anton’s estate will be taxed as assets passing to his sons are not exempt transfers for inheritance tax. Anton’s estate can use his full Nil Rate Band (£325,000), and the Residential Nil Rate Band (£150,000) as his main residence passes to his direct descendants. Therefore, Anton’s estate is taxed on £525,000 at 40%, meaning that inheritance tax of £210,000 is due before assets can be distributed.

Example 3 – Married partner with children and step-children

Nicola died recently leaving her surviving spouse Katherine; Nicola had a child Tom, from a previous relationship; Katherine has a son Colin, also from a previous relationship. Nicola’s estate is valued at £1,500,000 but she did not own their house, which was owned by Katherine.

Under intestacy rules, Nicola’s assets will pass as follows:

- £270,000 passes to Katherine

- The remaining £1,230,000 is divided between Katherine and Tom:

- £615,000 passes to Katherine

- £615,000 passes to Tom

- £0 passes to Colin

It is unlikely that this split of assets would have been what Nicola would have wanted. Effectively, the rules of intestacy would leave Colin without any legacy from Nicola.

Nicola’s estate will be taxed as assets passing to her son are not exempt transfers for inheritance tax, although assets passing to Katherine would be exempt transfers. Nicola’s estate can use her full Nil Rate Band (£325,000). Therefore, Nicola’s estate is taxed on £615,000 at 40%, meaning that inheritance tax of £116,000 is due before assets can be distributed.

Making a will – inheritance tax benefits

Control over your assets

If you make a will, you get to decide how your assets are distributed after you die. Your will allows you to retain control over how your assets are dealt with, but it can also give you peace of mind that your loved ones will be provided for.

This is especially true if you are not married, or want to allow for assets to pass to step-children. See the rules on intestacy (above).

By making a will, you can make specific gifts for certain people, and ensure that money eventually ends up with the right people.

Inheritance Tax efficiency

A key benefit to making a will is the ability to avoid inheritance tax. Wills are a great way that you can put your tax affairs in order so you can ultimately shelter assets from inheritance tax. For example, you may use your will to make gifts that use up your inheritance tax allowances, or to set up trusts.

You can also make sure that all the available inheritance tax exemptions are used at the right time, for maximum efficiency.

Practical issues

In practical terms your will enables your affairs to be put in order so your family does not have to do this after you are gone. Your will should ensure that the money ends up with your family more quickly. You will can make specific provisions to pay the inheritance tax due on gifts, or on the residuary estate.

This can resolve unnecessary complications after your death, since if you do not make it clear which gifts pay tax, your estate may create unforeseen issues.

Setting up a trust in your will

Your will can set up a trust that comes into force after your death. For example, you may choose to set up a fund for the benefit of a dependant, perhaps a child. Assets can pass as part of your will into the ownership of a trust. This can have inheritance tax implications as assets that pass to non-spouses will not be exempt transfers. Therefore, you need to consider whether any gifts that are made in your will are subject to inheritance tax or not.

Example 1

Julie recently died, leaving an estate valued at £1 million. In her will, she left £250,000 on trust to her son. Mark, with the remaining estate to her husband Colin. Because Mark is only aged 10, the gift to him was set up as a trust, which he will benefit from when he reaches age 18.

- The gift to the trust for the benefit of Mark is a non-exempt transfer

- The gift to the trust will use up £250,000 of Julie’s nil rate band for inheritance tax

- The gift to Colin is an exempt transfer, as Colin was Julie’s spouse

In this case, Julie’s estate will not pay inheritance tax because the gift to the trust would be below the current nil rate band (£325,000). £75,000 of this nil rate band (23%) would pass to Colin as Julie’s spouse. The remaining transfer of £750,000 to Colin is covered by the spouse exemption, meaning no inheritance tax should be due.

Example 2

If Julie had split her estate equally between Colin and Mark, then the full nil rate band would be used for the gift to the trust. Julie’s estate would be liable for the gift to the trust once the nil rate band is used up. Tax would be due on 40% of this excess, which would be £175,000 x 40% = £70,000. The will would usually stipulate whether the gift to the trust is paid free of inheritance tax, or not. If this were the case, then the residue estate would have to pay the tax due, and Simon would receive £430,000 (after the £70,000 inheritance tax is paid).

Which assets pass outside of your will?

Assets can be liable for inheritance tax but pass to people regardless of the provisions in your will. Some assets pass outside of your will, and are not liable to inheritance tax.

Assets that are liable to inheritance tax but pass outside of your will

- Property

Property tends to be owned under a “joint tenancy” although this is not always the case. What this means is that when you die, your share of the property passes to the remaining joint owners. In a normal couple situation the surviving partner receives the deceased person’s share outside of the will. However, the value of the asset is still taken in into account for inheritance tax. if the surviving partner is not married, then this transfer would be a non-exempt transfer for inheritance tax, meaning that tax might be due. - Joint assets

Other jointly-held assets also pass to the survivor(s) in the way described with the property above. This commonly applies to joint bank accounts, and other investments. Again, you should take care if the assets are held jointly with non-spouses as these could be liable to inheritance tax irrespective of the will. - Business assets

The treatment of business assets will vary according to the legal status of the business, and the arrangements made by the business owners. Often business assets may pass outside of your will, but are still taxable. You should check your arrangements in this area.

Assets that are usually free of inheritance tax but pass outside of your will

- Pensions

Pension plans are usually held in a kind of trust where the scheme trustees get to decide the ultimate beneficiary of the account. You should set up an “expression of wishes” which will guide the trustees as to your intentions after you die. In almost all cases, these wishes will be followed, unless you make a declaration that excludes an obvious dependant. For the purposes of inheritance tax pension funds are almost always passed free of inheritance tax. The only exception to this is if the pension was transferred within 2 years of death, and this is deemed by HMRC to have increased the death benefits payable. There are no published rules from HMRC on the subject but an obvious example might be where someone transfers out of a defined benefits (final salary) pension to a personal pension when they find out about a terminal illness. - Life policies

Life assurance policies will pass to the beneficiaries outside of your will if they are written for the benefit of another person, or to a trust. If your life assurance if written with you as the owner, then the proceeds will pass to your estate and form part of your will.

Deed of Variation – changing a will after a death

You can avoid Inheritance Tax by changing someone’s will after their death. This is known as a Deed of Variation.

Any changes to the deceased’s will must be agreed by all beneficiaries who may be left worse off, and must take place within 2 years of the death.

You can use a Deed of Variation to amend the will, perhaps to avoid Inheritance Tax more efficiently:

- Gifts using exemptions, to beneficiaries or trusts

- Gifts that qualify for reliefs to non-exempt beneficiaries

A Deed of Variation is a complex arrangement, so you need legal advice to be sure this is done correctly.

Spending more money to avoid Inheritance Tax

One reason that people accumulate enough money to create an inheritance tax liability is due to the fact that they have good savings habits. If you regularly spend less than your income, you will gradually save money and build up assets over time. This is a difficult habit to break, and we often see people with more money than they need, who still save money because they do not spend all of their income or capital.

Spending more income

One way to stop your estate getting bigger, and creating a larger inheritance tax bill is to make sure you spend all of your income. This will improve your lifestyle, and also help you to make sure that you pay less inheritance tax as you stop your assets from growing.

Accessing your capital

You can also spend your capital and savings to reduce your inheritance tax liability. You could regularly access your capital, thus reducing the value of these assets, or at least stopping them from growing over time. If you spend this money, it will help you to reduce the inheritance tax you pay. Just be aware that selling certain assets can trigger other taxes, such as capital gains tax.

Planning to spend more income or capital

Your overall goal should be to ensure that you reduce your inheritance tax liability but also ensure you never run out of money. Therefore, you should be careful not to deplete your assets too quickly. One way to be sure of this is to work with a financial planner like us, to help you to establish a safe withdrawal rate from your income or capital.

Lifetime Gifts for Inheritance Tax

You can make as many gifts as you like during your lifetime. Making gifts can be the best way to reduce the value of your estate and therefore is a good way to avoid inheritance tax.

Of course, you may feel nervous about giving away your assets while you are still alive since you may feel you could need the money in the future. With careful financial planning you can work out how much you can afford to give away to avoid inheritance tax and still have enough left over to fund your future lifestyle.

Exempt gifts

Certain gifts are exempt from inheritance tax. We explore these exemptions in the section below (“Inheritance tax exemptions”).

Potentially Exempt Transfers (PETs)

Most lifetime gifts that are not exempt from inheritance tax are known as potentially exempt transfers (PETs). If you make a lifetime gift which is not exempt from inheritance tax then no tax is usually payable at the date of the gift.

Potentially Exempt Transfers are useful tools for inheritance tax planning because they allow you to reduce the value of your estate. If you can justify making enough Potentially Exempt Transfers, and survive for long enough, then you can reduce or even remove inheritance tax entirely.

Potentially Exempt Transfers and the 7-year rule

When you make a Potentially Exempt Transfer the gift is ignored for inheritance tax provided you survive for 7 years from the date of the gift (known by many as “the 7-year rule”). The value of the lifetime gifts is not important, and will only be an issue if you do not survive for 7 years.

Benefits of Potentially Exempt Transfers

- The growth on the lifetime gift is immediately outside of your estate

Over time, the value of the asset given away is likely to rise, thereby increasing the future inheritance tax due. By giving away the asset, the future growth is outside your estate for inheritance tax purposes. Effectively, your estate is no worse off by making the lifetime gift, even if you do not survive for 7 years. - Complete inheritance tax avoidance after 7 years

- Tapering of the Residential Nil Rate Band

Estates valued over £2 million, will gradually lose the Residential Nil Rate Band (see above). If you make a Potentially Exempt Transfer you can immediately regain the Residential Nil Rate Band, even if the full 7 years have not passed to make the gift effective for inheritance tax.

Taper Relief and Potentially Exempt Transfers

If you make a lifetime gift, but do not survive for 7 years, then the gift will drop back into your estate for inheritance tax. Gifts up to the Nil Rate Band (£325,000) are not taxable, but the net result will be that other assets in your estate will instead pay inheritance tax.

Taper relief and gifts over £325,000

Where the total value of lifetime gifts in the 7 years prior to death was over £325,000, the excess can attract Taper Relief as set out below:

| Years following gift and death | Reduction in inheritance tax | Effective rate of inheritance tax on the gift |

|---|---|---|

| Fewer than 3 years | 0% | 40% |

| 3 to 4 years | 20% | 32% |

| 4 to 5 years | 40% | 24% |

| 5 to 6 years | 60% | 16% |

| 6 to 7 years | 80% | 8% |

| 7 years or more | 100% | 0% |

Taper relief and gifts less than £325,000

If the gift was less than £325,000 then taper relief does not apply. Instead the value of the gift will reduce the available Nil Rate Band. For deaths within 7 years of the date of any gifts less than the Nil Rate Band the Inheritance Tax will be the same as what would have been paid had the gift not been made. Any growth on the value of the asset gifted will not be taxed. In practice, this could mean that the inheritance tax may not be payable on the gift, but could instead be applied to other assets which pass to alternative beneficiaries.

Example of a gift lower than the taper relief threshold

Sandra owns £1,000,000 in cash. She gives £100,000 to her son John, and then dies 6 months afterwards.

Her will leaves the remaining £900,000 to be split equally between her 2 children John and Stuart.

Because there was less than 7 years between the gift and her death, then the gift to John is brought back into Sandra’s estate. Sandra died less than 3 years after making the gift, but did not benefit from taper relief. The gift to John is tax-free, and used £100,000 of Sandra’s Nil Rate Band.

The remaining estate of £900,000 can only benefit from £225,000 of Sandra’s Nil Rate Band (£325,000 less £100,000). This means Sandra’s remaining estate is taxable on £675,000 at 40%. Sandra’s estate will pay Inheritance Tax of £270,000, which will be deducted from the £900,000 remaining cash before distribution to John and Stuart.

John and Stuart will each receive £315,000 after deduction of inheritance tax. Of course, John also received £100,000 in addition from the gift that was not taxed.

What this means in practice is that when compared to the Inheritance Tax position before the gift, the same tax was paid. Unfortunately for him, Stuart ended up bearing a larger proportion of the tax bill compared to his legacy received.

Insurance and taper relief

You can insure the potential Inheritance Tax liability on any gifts that are greater than £325,000, and potentially subject to taper relief. This is known as a gift inter vivos life assurance (see below)

Gifts out of normal income

Since you have already paid tax on your income you can give away any excess without paying inheritance tax. This must be done carefully to avoid inheritance tax effectively. You should document your gifts carefully, and it should be clear that your lifestyle is being funded from the retained income. This means that you must be able to maintain your lifestyle from your income after making the gift. If you give away amounts from your income you cannot rely on capital to fund your expenses.

Example of gifts out of income

Marsha has an income of £60,000 per year. Once income tax is deducted, she is left with £45,000. Her annual expenses are £35,000. Therefore, Marsha can afford to give away £10,000 each year without any impact on inheritance tax rules.

Marsha would not be allowed to give away £15,000 as a gift from income, if she also used £5,000 capital withdrawals from her savings to make up the difference.

Gifts lower than market value

You may be tempted to think that you can pass on assets for less than they are worth, and this might get around the rules on inheritance tax. Unfortunately, if you sell any assets for less than their market value (losing value as a result) then the difference will count towards the value of the gift for inheritance tax.

Example gift lower than market value

Bob owns a valuable painting worth £100,000. He decided to “sell” this painting to his daughter Jane for £1,000 thinking that this transaction will mean that the painting will not form part of his estate in his inheritance tax calculations. This is wrong, and Bob’s estate would be treated as making a gift of £99,000 to Jane, which would reduce Bob’s Nil Rate Band if he were to die within 7 years.

Gifts with reservation of benefit

In the past some people tried to get around the Inheritance Tax gifting rules by giving away assets but still continuing to enjoy the use of them. This is known as gifts with reservation of benefit. If a gift with reservation of benefit occurs then the gift would still be treated as part of the estate of the deceased, even if they no longer own the asset on death.

Example

Shaun owns the house he lives in. He decides to “give” this house to his daughter Stacey, and then Stacey “generously” offers to let Shaun live there rent-free. This transaction would be treated as a gift for inheritance tax purposes, and also legally. This would mean that while the house might legally pass to Stacey (leaving Shaun less than certain of his future housing prospects), the value of the gift would still be counted when Shaun dies. This is because Shaun has reserved the use of the asset.

Gifts with reservation of benefit and market rent

The only way around the gift with reservation of benefit rules is to pay a market rent on the asset after making the gift. If, using the above example, Shaun paid Stacey a fair market rent for the use of the house, this would be treated as a Potentially Exempt Transfer from the start of the rental payments.

Using equity release to fund gifts

One method to help avoid inheritance tax could be to use equity release (otherwise known as a lifetime mortgage). This allows you to access the equity in your property, which could then be used to fund a lifetime gift to your family, or to a trust. The usual inheritance tax gift rules apply.

How does equity release work?

Equity release allows you to access some of the equity in your home, based on the value of that asset and your age. The lender will give you a cash balance to spend as you would like, and will charge interest on this cash. The interest will roll up against the value of the property, and will be repaid when you die, or perhaps sell the property to fund care costs. There will be a guarantee in place to ensure that the debt is never greater than the value of the property, so the family will not fall into negative equity. For this reason, the younger you are, the lower the amount that the lender will be prepared to release.

How does equity release work for inheritance tax planning?

Equity release could work in certain inheritance tax situations, especially where the majority of your assets are tied up in property.

If you can release equity from your home, you can then spend this, or give it away. This should reduce the value of your estate for inheritance tax purposes (provided you survive for 7 years from the date of the gift). In turn, this could allow you to reduce the inheritance tax bill. The equity release is a debt on the estate and must be repaid on death.

Barbara’s story

Barbara is single and holds a house worth £500,000. She also has savings of £200,000. She estimates that her estate’s inheritance tax bill after her death will be £80,000. Barbara could give away her savings, but she wants to retain the use of this money. Another solution is to take equity release of £200,000 from her home. Provided she lives for 7 years from the date of this gift her estate will reduce to £500,000, leaving her inheritance tax bill at £0. Of course, asset values could change over this period.

Advantages of equity release for inheritance tax planning

- Access to property assets for gifts

- Creates a debt against the estate, reducing its value for inheritance tax

- You can stay in your home

- No monthly interest costs

Disadvantages of equity release for inheritance tax planning

- The interest cost tends to be greater than standard mortgages

- The debt will rise over time

- If you want to move house the debt must be repaid

- The interest costs could be greater than the inheritance tax saved by making gifts, especially if you do not survive for 7 years

Logging inheritance tax gifts

If your gifts are aimed at avoiding inheritance tax, it makes sense to document these gifts. The alternative is that your family is likely to have to sort through your documents after your death to prove how much was given away, and that no tax is due on those gifts. This can be an onerous task, especially if there are many gifts, and they started years before your death.

Logging inheritance tax gifts – an easy method

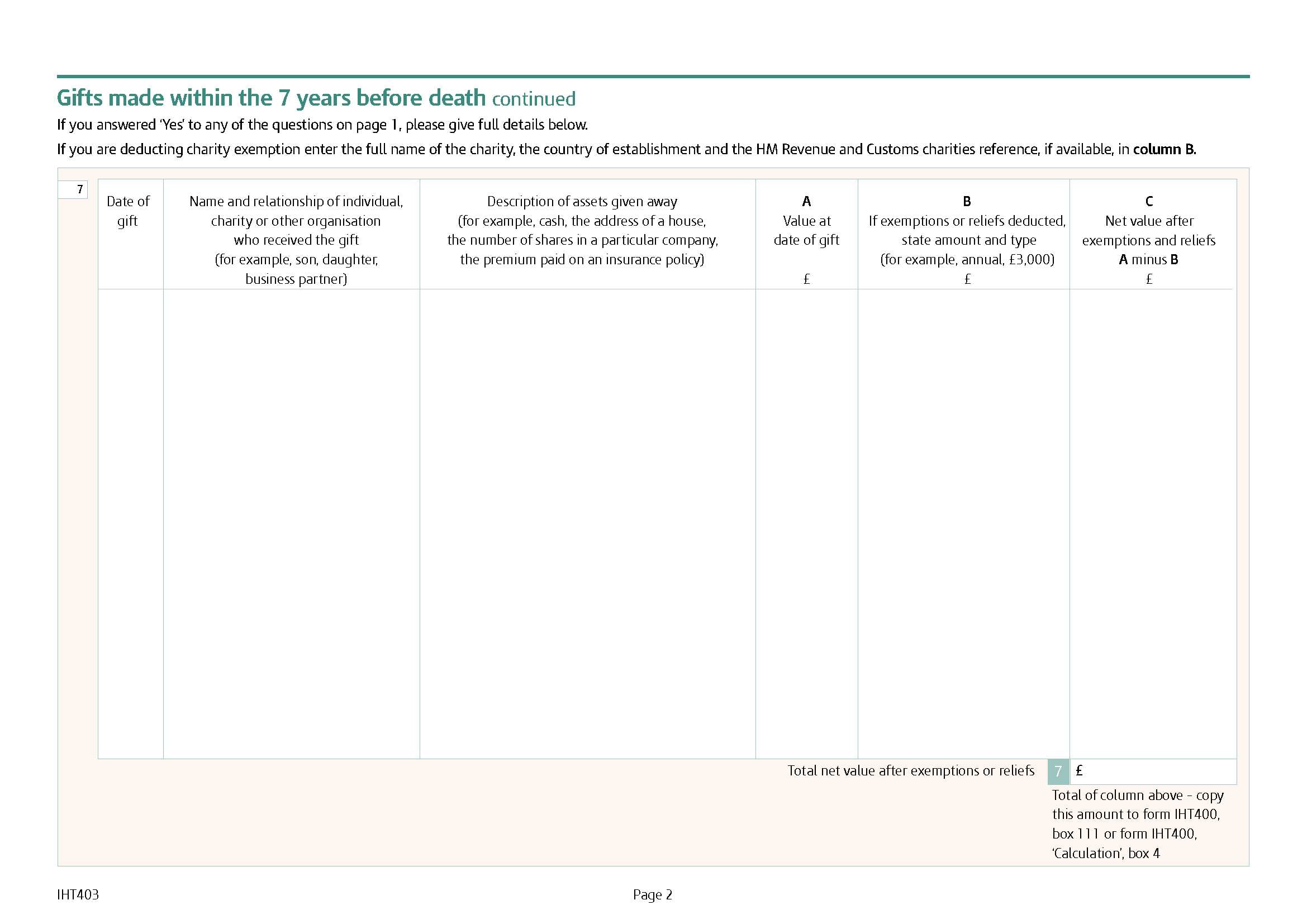

When logging inheritance tax gifts, it makes sense to look at the information that your personal representatives will be expected to provide in order to obtain probate (control over the assets after your death). This is declared on an official form called the IHT 403.

This inheritance tax form is helpful while you are making the gifts, as it shows you the data that HMRC will need. A straightforward solution is to keep a copy of this form with your important papers, and log the gifts as you make them, along with evidence such as bank statements. If your personal representatives can easily complete this form, the calculation for inheritance tax should be relatively easy (and your estate is less likely to be investigated).

Lump sum inheritance tax gifts

If you have made inheritance tax gifts that could be chargeable if you die within 7 years, log these on page 3 of the IHT 403 form.

This asks for the following information:

- Date of the gift

- Name and relationship of the individual/charity/organisation who received the gift

- Description of the assets given away

- Value on the date of the gift

- Any inheritance tax exemptions applied (such as the annual exemption of £3,000)

- Net value of the gift after exemptions or reliefs

Keeping associated records would be sensible, such as valuations, statements etc.

Gifts out of normal income

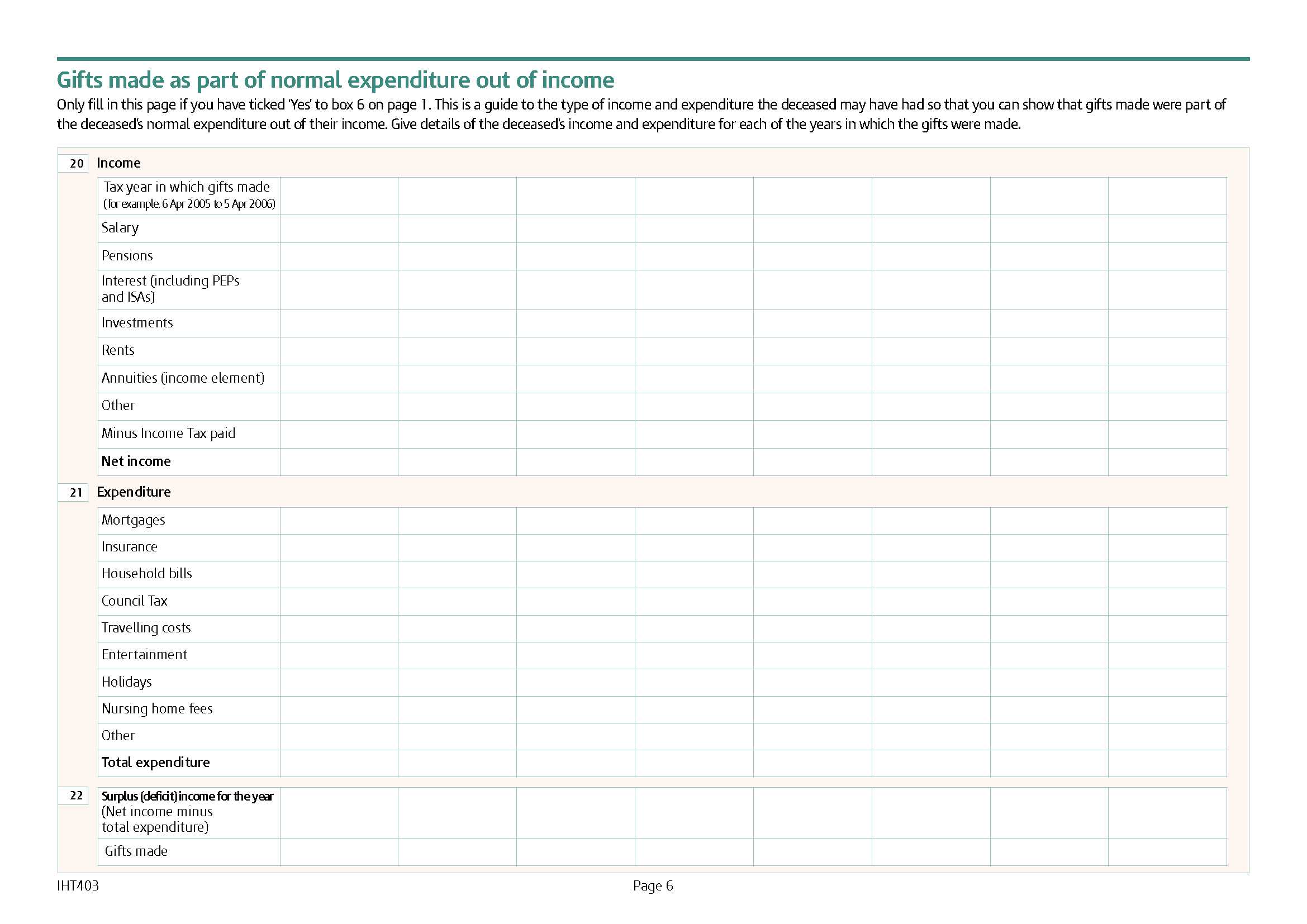

If you have made inheritance tax gifts out of income, these should be exempt from inheritance tax, since you have already paid income tax on this money. However, be careful not to give away money from income if you then need to dip into capital to fund your lifestyle. HMRC would deem that these gifts are instead gifts from capital, and could be liable to inheritance tax as set out in the previous section. Log these on page 8 of the IHT 403 form.

This asks for the following information, split as totals for each tax year:

- Tax year when gifts were made

- Breakdown of your income for that tax year

- Breakdown of your expenditure for that tax year

- Surplus income left over for that tax year – this is what can be given away

- Gifts made in the tax year

Again, we recommend that you retain records for this information, although this is unlikely to be checked. This might include tax returns, bank statements, budgets etc. You should also write a simple letter to whoever receives the gift to declare your intentions.

Inheritance Tax Gifts and Capital Gains Tax

If you make gifts to avoid Inheritance Tax, you must also be aware that some transfers of assets are subject to Capital Gains Tax while you are still alive. You should be careful not to make gifts intended to avoid Inheritance Tax only to find that they are chargeable to Capital Gains Tax. Read more about Capital Gains Tax on Investments.

What is Capital Gains Tax?

Capital Gains Tax applies to the sale or disposal of non-exempt assets. Usually, this applies to assets like investments, valuables, or rental property. Capital Gains Tax does not apply to your main residence.

In the context of Inheritance Tax gifts, you may give away a valuable asset such as a rental property. If this is not sold for a market value, then the value of the gift is likely to be assessed for Capital Gains Tax. The first £6,000 of gains per person in a tax year are tax-free. After that, gains are added to your income for the tax year. Any gains in the basic rate income tax band are taxed at 18% for property, and 10% for other gains. Any gains that fall into the higher rate income tax band are taxed at 28% for property, or 20% for other gains.

Inheritance tax and capital gains tax example

Lee has a total estate valued at £1,000,000. He decides to reduce the value of his estate by giving away taxable investments worth £100,000 to his son Mike. Lee calculates that after 7 years this will save his estate £40,000 in inheritance tax.

Lee later finds out that he should have paid capital gains tax on the growth to his investments. He establishes that his investments initially cost £40,000. This means he has a gain of £60,000. After taking away the annual allowance, this leaves a taxable capital gain of £54,000.

Lee is a 40% (higher rate) income tax payer. Therefore, the capital gains tax on the gift to Mike is £10,800.

Inheritance Tax exemptions, allowances and reliefs

You can use a variety of exemptions, allowances and reliefs to avoid Inheritance Tax. These are useful because they do not affect your Nil Rate Band for Inheritance Tax.

Inheritance Tax exemptions and allowances

Use inheritance tax exemptions

Certain gifts are exempt from inheritance tax. These include the following:

- Gifts to spouses

As previously mentioned, anything you give to your spouse during your lifetime or on death is free of inheritance tax. Of course, when your spouse dies inheritance tax could still be payable. However this can be useful to avoid inheritance tax especially when one spouse is younger than another. - Annual exemption

You are permitted to give away up to £3,000 in any one tax year without attracting inheritance tax. If you have not used this allowance in the previous tax year you can bring this forward for 1 year only. Thus, you could double this up to £6,000. If you are part of a married couple you could give away £12,000 in one tax year. - Small gifts

You can give away up to £250 as many times as you like to as many people as you want. - Wedding gifts

There are rules around gifts to children or grandchildren on consideration of marriage. Certain amounts can be given away without attracting inheritance tax. - Gifts to charities or political parties

You may give as much money as you want to charities or political parties and effectively avoid inheritance tax. Gifts to charities in your will also reduce the Inheritance Tax rate to 36% provided 10% of the “net estate” is passed to charity.

- Gifts to spouses

Small gifts

There is no inheritance tax to pay on small gifts. You can give away up to £250 at a time to as many people as you want in a tax year, without incurring any inheritance tax.

Wedding gifts

You can give wedding gifts without incurring inheritance tax as follows:

- £5,000 to your child

- £2,500 to your grandchild

- £1,000 to anyone else

Payments towards someone’s living costs

You can make regular payments to help with another person’s living costs. This might include an elderly relative, or a child under 18.

Gifts to charities or political parties

These are exempt from inheritance tax.

Using multiple inheritance tax exemptions

You can combine the inheritance tax exemptions. For example, you could give away money towards a wedding, to a charity, under the annual exemption, and further small gifts. Provided each of these gifts was within each limit then no inheritance tax would be due on them. Of course, it makes sense to carefully document your inheritance tax gifts.

Inheritance Tax Reliefs

There are other Inheritance Tax reliefs available. These may not be 100% exempt from inheritance tax, but can provide relief from tax either partially, or fully after conditions are met.

Business Relief

You can get Business Relief (also known as Business Property Relief) on ownership of a business, or shares in a qualifying business. This can be claimed at either 50% relief or 100% relief. This relief is based on the market value of the business.

To qualify for Business Relief the deceased must have owned the qualifying assets for at least 2 out of the last 5 years prior to death, and at the date of death.

Business Relief can be claimed on:

- Business property and buildings – 50% relief available

- Unquoted or unlisted shares – 100% relief available

- This also includes AIM listed shares and Enterprise Investment Schemes (EIS)

- Shares controlling more than 50% of the voting rights in a listed company – 50% relief available

- Machinery – 50% relief available

Business Relief cannot be claimed on:

- Not-for-profit companies

- Companies that mainly deal with securities, stocks or shares, land or buildings, or in making or holding investments

- Companies that are being sold unless shares in the company buying the shares issue shares as payment

- Companies being wound up

Partially qualifying for Business Relief

Your assets may partially qualify for Business Relief if a non-qualifying asset forms part of a qualifying asset. For example, if your property is used as a home, but part of that home is a business, then the business may qualify for Business Relief, but the home would not. Business Relief would be apportioned as a percentage of the value of the overall asset.

The ownership test

Business Relief can be passed between assets in certain circumstances. This can include where the business property was acquired as a result of the death of another person, or where that transferred property replaced other business property.

Example Business Relief

Miriam set up her business as a limited company (which was privately owned) and held all of the shares. When she died, she left the shares to Aaron, her son. Because the shares were unlisted, and held for more than 2 years to the date of Miriam’s death, the asset will qualify for 100% Business Relief against inheritance tax.

Investments and Business Relief

Certain investments exist which aim to allow you to buy into a scheme that qualifies for Business Property Relief. This is useful where you want to retain control over the assets purchased (in case you need to sell at some point), but also aim to qualify for 100% relief against Inheritance Tax. We have recommended such schemes for elderly clients who want to benefit from Inheritance Tax relief after 2 years, rather than to wait for 7 years if they make a gift.

These investments often come with additional risks. See below for more details of Business Property Relief Investments.

Agricultural Relief

Some agricultural property can qualify for relief against Inheritance Tax. Agricultural property must have been owned for at least 2 years prior to death if occupied by the owner, their company, or spouse or civil partner. If this does not apply, the period of ownership must be 7 years prior to death.

Assets qualify for Agricultural Relief at 100% of their value if:

- The person who owned the land farmed it

- The land was farmed by someone else under a short-term grazing licence

- The land was let out under a tenancy began after 1 September 1995

Other cases qualify for Agricultural Relief at 50%.

The following property qualifies for Agricultural Relief:

- Land or pasture used to grow crops or to rear animals

- Stud farms for breeding and rearing horses and grazing

- Trees that are planted and harvested at least every 10 years (short-rotation coppice)

- Land not currently being farmed under the Habitat Scheme

- Land not currently being farmed under a crop rotation scheme

- The value of milk quota associated with the land

- Some agricultural shares and securities

- Farm buildings, farm cottages and farmhouses

The following property does not qualify for Agricultural Relief:

- Farm equipment and machinery

- Derelict buildings

- Harvested crops

- Livestock

- Property subject to a binding contract for sale

Business Relief and Agricultural Relief combined

You cannot claim Business Relief on the value of any asset you have already claimed Agricultural Relief on.

Inheritance Tax Insurance

Inheritance tax insurance is not really a way to avoid inheritance tax – it is more a way to ensure that the liability is funded when you die.

You can set up a whole of life insurance plan which will pay out a lump sum on your death. This will then pay the Inheritance Tax due at that point. If done correctly, the net result is that your relatives will receive the amount they expect, but the policy will pay the tax due. Of course, you should write this policy in trust to ensure that the tax situation is not made worse.

The downside of this approach is that there is a cost to the cover, which can be significant as you get older. However, the main advantage is that it is a simple solution which leaves you in full control of your assets while you are alive.

What is inheritance tax insurance?

Inheritance tax insurance is a type of whole of life insurance cover. You can set up an insurance policy to pay out a lump sum on your death. The idea is that with this whole of life insurance policy you will be able to fund the inheritance tax you owe rather than avoid paying inheritance tax. You can use alternative types of life insurance, such as term assurance. However, the danger of this approach is that term assurance runs out after a set period. If you live longer than that term, you risk not being able to set up or afford new cover, leaving your Inheritance Tax planning to fail.

Whole of Life cover is guaranteed to pay out the sum assured, provided you maintain the cost of the cover during the lifetime of the policy. Of course, the longer you live, the higher the cost. in general, the older you are when the Inheritance Tax Insurance starts, the more expensive it will be.

You pay for the insurance while you are alive and it will provide your family with the lump sum to pay the inheritance tax on your death.

An example

John and Linda are both in their early 70s. They have a combined estate for tax purposes of £1,500,000 made up of their house, savings and investments. They know that when either of them die, their estate will pass to the survivor. However, on second death their children will need to pay inheritance tax as follows.

Value of estate on second death = £1,500,000

Inheritance tax threshold on second death = £950,000

Taxable estate = £550,000

Inheritance tax payable at 40% = £220,000

John and Linda could make gifts of £550,000 to their children and hope to survive 7 years from the date of these gifts. However, they prefer to retain control over their assets, as they need the income from them and may need to fund future care costs.

Instead, they set up a whole of life inheritance tax insurance policy designed to pay the £220,000 tax liability on second death.

Why consider inheritance tax insurance?

Here are some good reasons to consider inheritance tax insurance:

A simple solution

Inheritance tax insurance is a simple solution to a complex problem. There are many ways to avoid paying inheritance tax (see above). The advantage of inheritance tax insurance is that it is straightforward. You can simply set up a policy with the knowledge that on your death the proceeds will pass to your family to be used towards your inheritance tax bill. You do not avoid tax with inheritance tax insurance – you provide the means to pay it.

Retain control over your assets

Inheritance tax insurance allows you to retain full control over your assets while you are still alive. In our experience most people put off doing something about their inheritance tax liability. This is usually because the solutions presented are too complicated, or because they worry that they might need the assets in the future. The advantage of inheritance tax insurance is that you do not need complex trusts or to give away assets. Instead you simply fund for the liability in the future.

Types of inheritance tax insurance

Inheritance tax insurance is whole of life insurance. This is a type of life assurance which guarantees to pay out a lump sum with no end date on it. therefore, if you maintain the policy payments you can be sure that it will pay out.

There are 3 main types of inheritance tax insurance:

Maximum cover

This is the cheapest form of cover in the short term. Usually what happens is that for the first 10 years of the plan your payments are kept low. Your payments will partly fund insurance and partly fund an investment portion of the policy. After a set period your policy will be reviewed and the payments reassessed based on the performance of the investment element. Since the initial payments have been set to be lower cost, it is likely that the costs will dramatically increase in the future.

Balanced cover

This works much like maximum cover, except that the initial costs are set at a more realistic long-term level. The policy is still dependent on the investment performance but it is much less likely that significant increases will occur in the future.

Guaranteed cover

This tends to be the most secure form of cover, but also the most expensive. Guaranteed cover sets the cost at the outset and this will not change in the future. Therefore, if you want to be sure that your inheritance tax insurance costs do not change, then this is the best option.

Term assurance

You could take out a cheaper form of life assurance called term assurance. Instead of running for the whole of your life, this cover instead runs for a specific term. This makes the cover cheaper, but also risks failure of your Inheritance Tax planning if you live longer than the term.

“Gift Inter Vivos” policy

A gift inter vivos policy is a 7-year term assurance that is used to fund the decreasing Inheritance Tax liability of a Potentially Exempt Transfer (see above). Potentially Exempt Transfers are Inheritance Tax gifts that only become chargeable to tax if you do not survive 7 years from the date of the gift. If you make a gift less than the Nil Rate Band (£325,000) then there will not be any Inheritance Tax to pay for the recipient (unless this is made as a condition on the gift). If the gift is greater than the Nil Rate Band then there is a tapered reducing Inheritance Tax liability on the value of the gift over that amount, between 3-7 years after the date of the gift.

A gift inter vivos life assurance policy can be used to fund the decreasing liability to Inheritance Tax. The policy proceeds can be written into a trust to pay out on the donor’s death, to fund any Inheritance Tax that becomes due.

Costs of inheritance tax insurance

As you can imagine inheritance tax insurance can be expensive, especially when significant liabilities need to be insured. However, if you are in a married couple (or civil partnership), you can make the policy cheaper by setting up on a joint life second death basis. The basic rule of thumb is that the older you are the more expensive it will be. Costs will also increase the greater the cover required.

Important considerations for inheritance tax insurance

Reviewing cover

You need to regularly review your cover. It is common for assets to grow at a faster rate than the inheritance tax threshold. What this means is that over time you inheritance tax liability could be getting bigger. Therefore, you need to build in regular reviews of your inheritance tax insurance so that you are sure that your cover is sufficient to cover your liability. Of course, any insurance is better than none.

Age

Inheritance tax insurance is cheaper the younger you are when you set up the policy. It is generally not available after age 80 at entry, although some policies can have up to age 85 at entry.

Health

If you have underlying health conditions this can make the policy more expensive or even mean that you are refused cover.

Trusts

Your inheritance tax insurance policy should be written into trust. If this is not done, your insurance will add to your estate on death and you will pay even more inheritance tax. By writing the policy in trust you will avoid inheritance tax on the proceeds and also allow your family to receive the money quicker. Your insurance company will provide you with free trust wording when you set up the policy.

First death or second death

In a married couple you would typically set up your inheritance tax insurance to pay out on second death since transfers between spouses on first death are usually tax free. However, you should take care with the set-up of your policy since inheritance tax can be a complex area.

Inheritance Tax Trusts

Trusts are an effective legal mechanism to help you to avoid inheritance tax.

You can make gifts to trusts, which may allow you to exercise some control over the assets. There can be tax advantages to gifts to trusts, but there is added complexity and cost involved. Trusts are taxed heavily, so you should only make gifts to trusts after taking advice. Otherwise you may find yourself avoiding inheritance tax only to end up paying an alternative tax. You may be able to place existing assets into trust to avoid inheritance tax (although such a transfer could attract income tax or capital gains tax). You can do this easily with pensions and life assurance. For example, most pension plans can be written into trust so that on your death the assets pass outside your estate and go straight to your relatives without paying inheritance tax. If you have set up life assurance you should put this policy into trust. This helps you to avoid inheritance tax as it excludes the value of the policy from your estate, and you therefore ignore the value for tax purposes.

Inheritance Tax Investments

With some careful planning you can effectively avoid inheritance tax. You can take out certain investment products, which have particular inheritance tax treatments. This can enable you to gain a potential income or future withdrawals from the product, while still removing money from your estate and thus avoiding inheritance tax. These schemes tend to be more complex, but can be extremely effective.

Set out below are some typically available Inheritance Tax Investments.

Business Relief Investments

Business Relief investments aim to use reliefs legally avoid Inheritance Tax.

How do Business Relief Investments work?

You can buy investments which buy shares in one or more privately owned companies. To be able to qualify for Business Relief from Inheritance Tax, these investments will not be listed on a recognised stock exchange, and must be owned for at least 2 years at the date of death. Therefore Business Relief investments aim to be free of Inheritance Tax after just 2 years, provided the shares continue to qualify.

Advantages of Business Relief Investments

- Avoid Inheritance Tax after just 2 years

- You own the asset

- You can sell some or all of the shares at any stage if you need access to the money (this will lose Business Relief and reverse the Inheritance Tax savings)

- All potential investment growth is outside of your estate

Disadvantages of Business Relief Investments

- Business Relief investments can be expensive

- However, the Inheritance Tax savings can be huge

- These investments are risky

- By their nature they invest in unquoted companies, which tend to be smaller, are less established, and can be difficult to value

- The shares may not be diversified, which also increases risk

- Capital and income can fall in value

- The investments may not be accessible

- As investments are not quoted on a stock exchange, you can only sell them if you have a ready buyer.

- The promoters may arrange for you to sell to a buyer, but this is not guaranteed

- Business Relief could be withdrawn at any stage (although has existed since Business Property Relief was started in 1976)

Business Relief investments and Lasting Powers of Attorney or Deputyship