Planning your retirement guide

This article explores all the issues you need to examine when planning for retirement. We aim to show you what you need to consider when planning for retirement so that you know you can afford to retire, without ever running out of money. You should read this if you are planning for your retirement but do not know if you can afford to stop working.

Who should read this Planning your Retirement Guide?

This information should be useful to you if you are planning retirement, even if this is many years away. If you are ready to retire, the information below will help you to decide if you can take the next step.

We also consider tricky technical details that you need to understand, so that you can make the most of the retirement tax rules available to you. This is particularly valuable if you are a business owner or have a high income.

- Planning your retirement

- Preparing to retire soon

- Tax-efficient pension savings

- Flexible pension income

- Pensions for business owners

- Tax issues for high earners

Key topics covered in this article

Click on the links in this table to go straight to that section of the Planning your Retirement Guide:

Planning your retirement – an overview

Before you start planning your retirement, you must first begin to consider what retirement means to you. This section of the Planning your Retirement Guide explores how to prepare for retirement the right way.

What is retirement?

Stopping work

For most people planning retirement, this means stopping work, and starting to do what you want to with your time.

Of course, your retirement will be individual to you and your circumstances. For many people your retirement is a positive experience where you get to regain your freedom. Of course, having enough money is vitally important when planning your retirement.

You do not have to stop work suddenly. With proper retirement planning you can gradually retire, possibly working part-time until you are ready to stop work completely.

“Retiring” from life

Another sense of retirement it is to withdraw from life. Younger people often view retirement negatively, seeing it as a withdrawal from work and other social activities. In fact, retirement is usually the opposite, provided you get your planning right. In our experience, provided you have done your planning, retirement can be a stage where you fulfill your dreams.

The ideal retirement?

We see retirement as having the resources to do things on your terms. If you have enough capital or income to be able to fund your lifestyle, then you can afford to stop working on your terms. If you continue working, you will only do so if it meets your needs, when you decide.

The ideal retirement is one where you have the freedom to meet your goals, and the financial resources to back this up. If you have financial stability you can focus on your lifestyle, relationships, health, and interests.

Planning retirement ultimately comes down to 2 factors:

- What will you do with your time?

- How will you pay for it?

Action:

- Take some time to seriously think about what retirement means to you.

- When planning retirement you should be thinking ahead to what life will be like after you stop working.

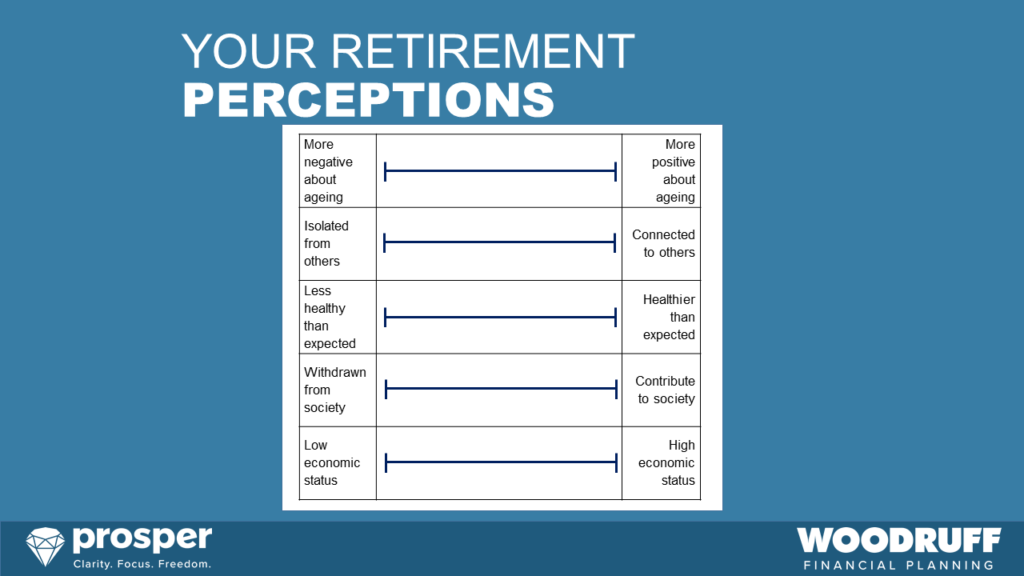

What will retirement be like?

Ask yourself what retirement means to you?

The answers to the questions below might help you to plan whether you are ready for retirement.

Rank yourself along the scales below. The further towards the right, the more positive you are likely to feel when planning retirement.

Our goal when planning your retirement is to aim towards the right of the scales set out above. The better you rank yourself against these measures, the more fulfilled your retirement is likely to be. Of course, you cannot control these areas fully, but you can do your best retirement planning to ensure the chances of success in these areas are greater.

A US academic study from 2016 found that those people with a more positive self-perception of aging lived on average 7.5 years longer than those with less positive self-perceptions of aging. When planning your retirement, the more positive you can be about the changes to your life, the better your chances for a longer life.

Planning your retirement – what will you do with your time?

One of the great benefits of planning your retirement is that you will get so much more free time. After all, if you no longer work, or work less, then more of your time will be yours. Of course, this works positively and negatively. You will move from a set routine into something less formalised. The danger of not planning your retirement is that you might allow your life to drift due to all the new-found free time.

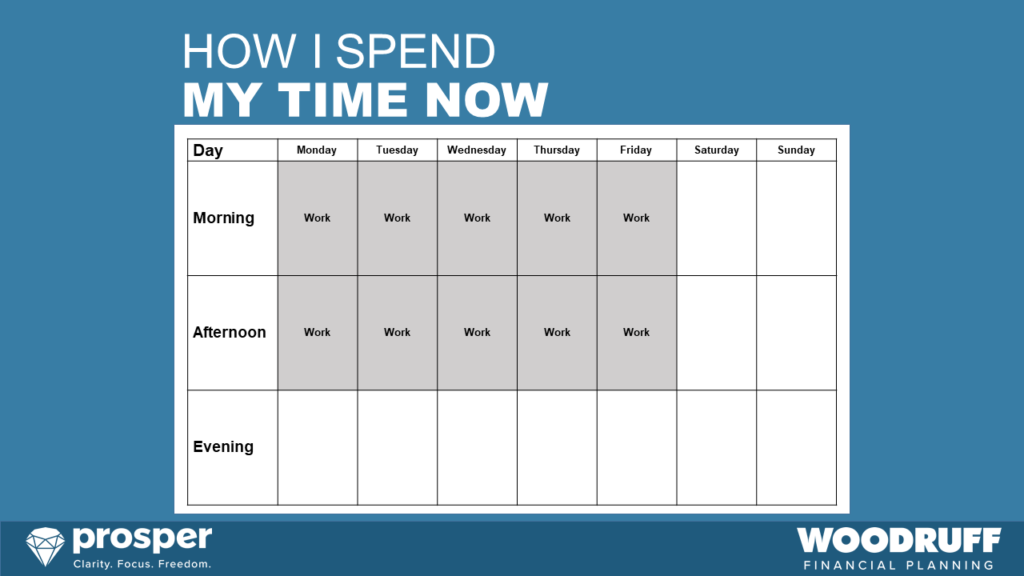

A simple exercise could be to examine how you spending your time before retirement, to how you might spend it after retirement.

How you spend your time now

This simple table shows the straightforward routine of standard full-time employment. Of course, your work routine may look different to this. You are used to following the routine of your work, and then filling in the blank areas with your interests, and family commitments.

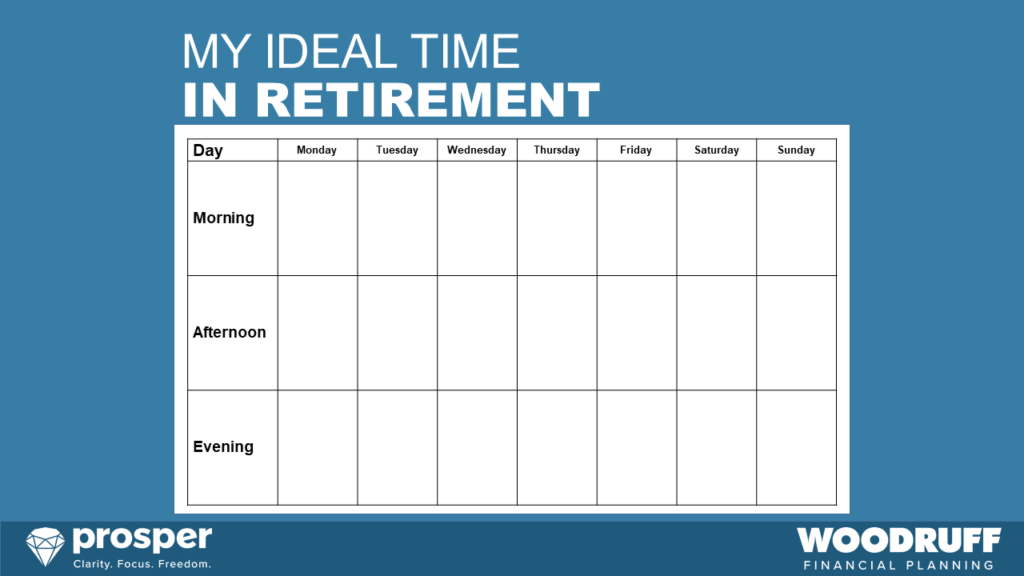

Your time after planning your retirement

When planning your retirement your goal is not to replace work with other commitments, but if you complete this exercise you might fill in the above chart with your future plans for hobbies, socialising, visiting family and other activities. One of the dangers of an unplanned retirement is that you become a magnet for others to fill your time. You might end up swapping the commitment and routine of paid work for unpaid commitments like child care, or volunteering. Of course, there is nothing inherently wrong with making such commitments when planning your retirement. However, we believe that you should only make such commitments in retirement on your terms.

Planning your retirement lifestyle

Various studies show the effects of various lifestyle choices during retirement. When planning retirement take care to be intentional about this, as the choices you make will have a bearing on the type of life you lead.

Physical exercise in retirement

The link between physical exercise and health is well-known, so it makes sense to apply this to your retirement plan. Various studies have linked this to better health in retirement. This study suggests that regular physical activity is associated with an increase of life expectancy by up to 6.9 years. If you can keep yourself relatively fit in your retirement, then not only will you live longer, but you are more likely to enjoy your retirement years.

Keeping your brain active in retirement

This study points to a survival example of reading every day, compared to other materials such as magazines. The general point is that if you keep using your brain, and solving problems, you are more likely to avoid the negative effects of aging on the brain.

Action:

- Consider your attitudes towards retirement – are you positive or negative about these issues?

- Establish an idea of how you will change your routine in retirement

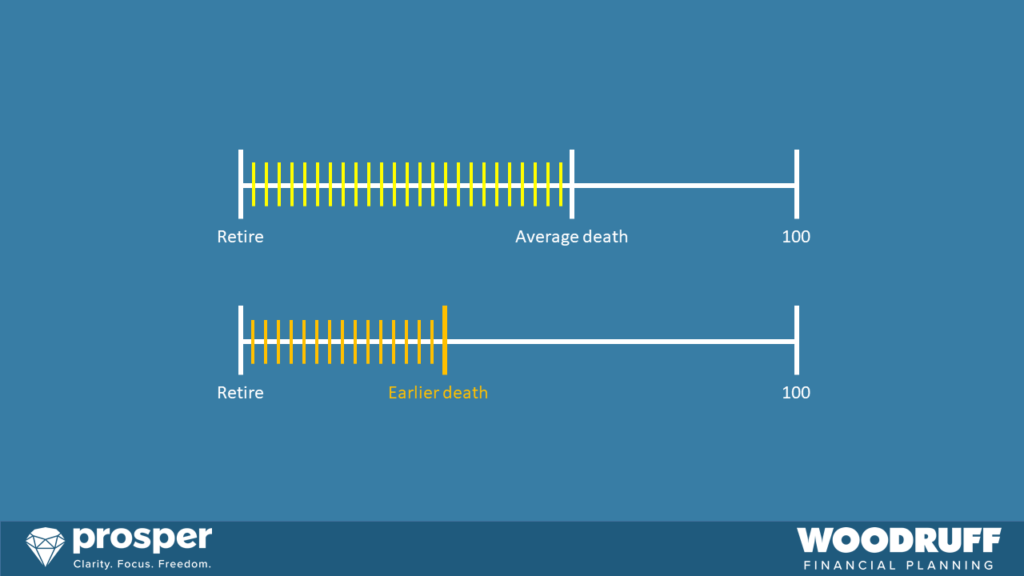

Life expectancy in retirement

How long you will live is a difficult question to answer when planning your retirement, but it is an important consideration even if it might be difficult to face. After all, we know that we are going to die one day, and our health might deteriorate before that event. Therefore, your task when planning your retirement is to focus realistically on this issue so that you can maximise the time you have while you are fit and healthy to enjoy retirement.

Life expectancy data

Life expectancy data is extremely important when planning your retirement. Essentially, the longer your lifetime then the more money you will need to fund your retirement expenses, especially if you plan to stop work or retire on a fixed income.

Make the most of your retirement

You should make the most of the time you have left, while you are still fit and able to do so. It is all too easy to ignore the future and worry about these issues later, even when planning retirement.

Life expectancy is lengthening

You may live a much longer life in retirement than you imagine. You cannot simply take a look at the lifespan of your parents or grandparents. We are all different, and medical advances are gradually increasing life expectancy. The advances in DNA mapping and data capacity should lead to a golden age for medical progress as scientists and doctors trace the causes of all illnesses. I expect this to lengthen everyone’s life expectancy in retirement, potentially at a much greater rate.

Prepare realistically for your future

Planning your retirement can help you to think about what resources you need to put aside to provide you with security for your future and a lifestyle worth living. Remember that longer life could mean coping with serious illness for a longer period.

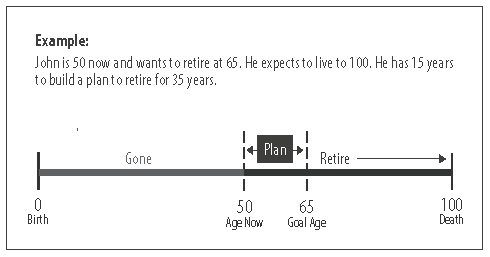

How long will you live? Your life expectancy and longevity as a timeline

Take a look at this timeline, which illustrates the point about life expectancy when planning retirement.

If you expect to live a long life then you need to work harder prior to retirement to provide the resources to fund for a secure and worthwhile future. Of course, if you expect to live a shorter lifetime then your retirement planning can assume you need lower capital.

We can apply this to retirement planning. You may think that you do not want to live to an advanced age, but that reality is more likely than you might think. And when you get there, the likelihood is that you may wish that you had prepared for a long lifespan.

Historical UK life expectancy data

The average life expectancy has been rising gradually, since 1850. Much of this is due to improvements over infant mortality, but medical advances now mean that the average retirement length has increased dramatically. Your retirement plan needs to consider this issue.

If you were born in an earlier age, your life would have been much shorter than today, and therefore your retirement would have also been shorter. The data above clearly shows that the average life expectancy in the UK was pretty low throughout the past 500 years. This was due to disease, famine, nutrition, medicine and war. Clearly, some people lived longer lives, but many died much younger. You can see a huge increase in UK life expectancy from the 19th Century as medical advances reduced disease.

Retirement planning: how to predict your life expectancy

The easiest way to predict life expectancy when planning your retirement is to use the statistical evidence. This can show you how long you will live based on the average. Of course, no-one is average, and your own retirement life expectancy will be determined by a variety of factors – genes, work history, exercise, food etc.

The statistics can lead to a certain complacency, or negativity, about your retirement life expectancy. For example, if the average life expectancy for someone at birth in the UK is now 86, you might use this figure in your Financial Planning. The reality is that this is the average figure. Half of the population will live longer than age 86.

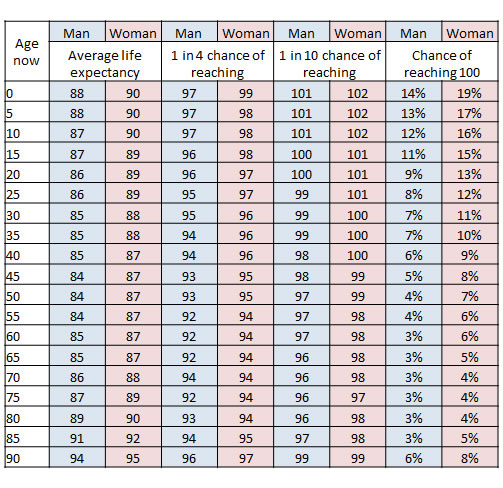

UK average life expectancy data

Here is a summary of life expectancy data from the Office For National Statistics.

How to read this data

This table shows results based on age now for men and women. If you examine the top row you will see that a child born today should expect to live an average lifespan of 88 for a boy, or 90 for a girl. That is the average, meaning half the children born today should expect to live longer.

The next 2 columns show that the same child has a 1 in 4 chance of living to 97 (boy) or 99 (girl). They have a 1 in 10 chance of living to 101 (boy) or 102 (girl). A new-born baby today has a 14% chance of living to 100 if it is a boy, or a 18% chance if it is a girl.

You can select the entry closest to your age on the left.

For example, if you are currently aged 60 your average life expectancy is 85 for a man, and 87 for a woman. A man who is currently aged 60 has a 1 in 4 chance of reaching age 92, and a 1 in 10 chance if reaching age 97. A woman who is currently aged 60 has a 1 in 4 chance of reaching age 94, and a 1 in 10 chance if reaching age 98.

You can get your own results using the Office For National Statistics life expectancy calculator.

Bear in mind that this data is for the whole population. It does not take into account other factors such as income, wealth, health and occupation.

The effect of health on life expectancy

Your retirement health will also have a major impact on your lifestyle. As we get older, we are more likely to have to deal with significant health issues. We believe you should look after your health where possible. This means taking regular exercise and eating well. However, we do need to face the fact that we are likely to have to deal with health issues in retirement. Therefore, why not maximise your opportunities while you are fit and able to do so?

Action:

- Consider how long you expect to live based on the data above – this will influence the amount of time your retirement money needs to last

The value of work when planning your retirement

No doubt you are planning your retirement partly because you want to stop working, or at least reduce your time in paid work. However, there is a value to work, not only in the financial sense, but also in the other benefits work brings.

Economic benefits of working

The economic benefits of working are obvious – you get a regular income. However, this can come with downsides, especially if you are self-employed.

Economic benefits of retirement

There are also costs of working that might reduce after retirement – for example commuting costs. In addition, if your retirement income reduces, so too will the effect of income tax.

Lifestyle benefits of working

The lifestyle benefits of working are important, but harder to quantify. For example, working brings a routine, which you might lose in retirement. There are social benefits to working from seeking a challenge, to meeting people, and solving important problems.

Lifestyle benefits of retirement

In retirement, you will gain more free time on your own terms. However, you may lose some important social aspects unless you replace your work with something else.

Action:

- Take some time to consider the relative advantages and disadvantages of working against the same issues if you retire. This will help you to establish whether retirement is important to you now, or perhaps can be delayed. Many people consider retirement not because they want to stop working; often the real reason is that they hate their job!

How will you pay for your retirement lifestyle?

On a practical note this guide to planning your retirement aims to answer this question. You must prepare ahead of your retirement for your expected budget, and then put together a plan for how you are going to pay to live in retirement. This section of the Planning your Retirement Guide considers what elements are important to paying for your retirement lifestyle.

When will you retire?

The date you plan to retire is very important. The earlier you retire, the less time you have to prepare for living from your resources, and the more you need to save to live off once your earned income ceases. The later you retire, the more time you have to build up reserves, but this will reduce the time you have to do what you want.

The decision of when to retire is important and should be taken carefully, since this can be irreversible if you leave your job.

Action:

- Think about when you want to stop working. Having an end date will help you to focus your attention and resources. If you conclude that you’re not ready to retire, that’s also fine.

Will you fully retire, or partially retire?

Traditionally, retirement meant ceasing work completely – that’s what the word means. Today, you have much more freedom to retire on your terms. You do not have to retire all at once, and you can plan your retirement in stages.

Actually, the decision to retire can be daunting. In many cases, you can ease yourself into retirement by partially retiring (also known as semi-retirement). That way you can see whether retirement agrees with you. Planning your retirement can take account of many options.

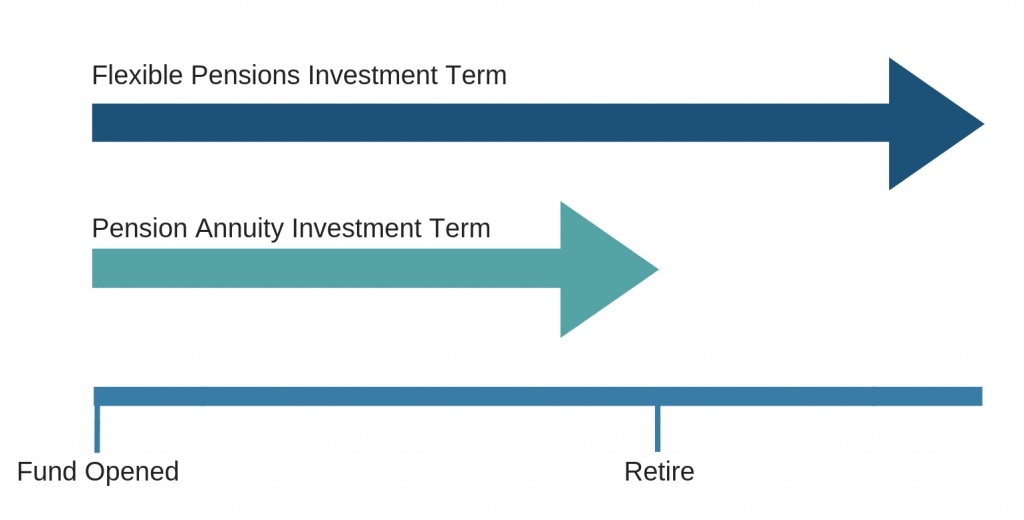

Taking retirement benefits gradually

Many people have a variety of retirement products and assets available to them. This could be personal pensions, defined benefits pensions, the state pension, investments or property (many other options exist). Some of these assets may have set dates for when the retirement income payments begin. Others give you more choice. This means that you need to plan when your income is to to start, and how it will be paid. The results can influence your decisions.

Example of taking retirement benefits gradually

Anita is aged 59. She has 3 retirement income sources:

- the state pension, which begins at her age 67

- A final salary pension, which begins at age 60 (some schemes allow you to change the start date)

- A personal pension which was set up to start retirement income at age 65, but in practice could begin income at any stage from age 55.

If Anita takes her retirement income based on these dates, her income pattern will change. This could influence her decision whether to continue working in her current employment.

Working less

Many people take the view that work is not the problem, but they want to work on their own terms as they approach retirement. You can partially retire, perhaps working fewer hours if you are employed, or taking on fewer clients if you are self-employed or a consultant.

Many employers are flexible with experienced employees, and might consider offering you a proportionate decrease in hours and salary. Self-employed workers can decide to take on fewer projects or clients, or wind down their client bank, so that they do not replace clients over time.

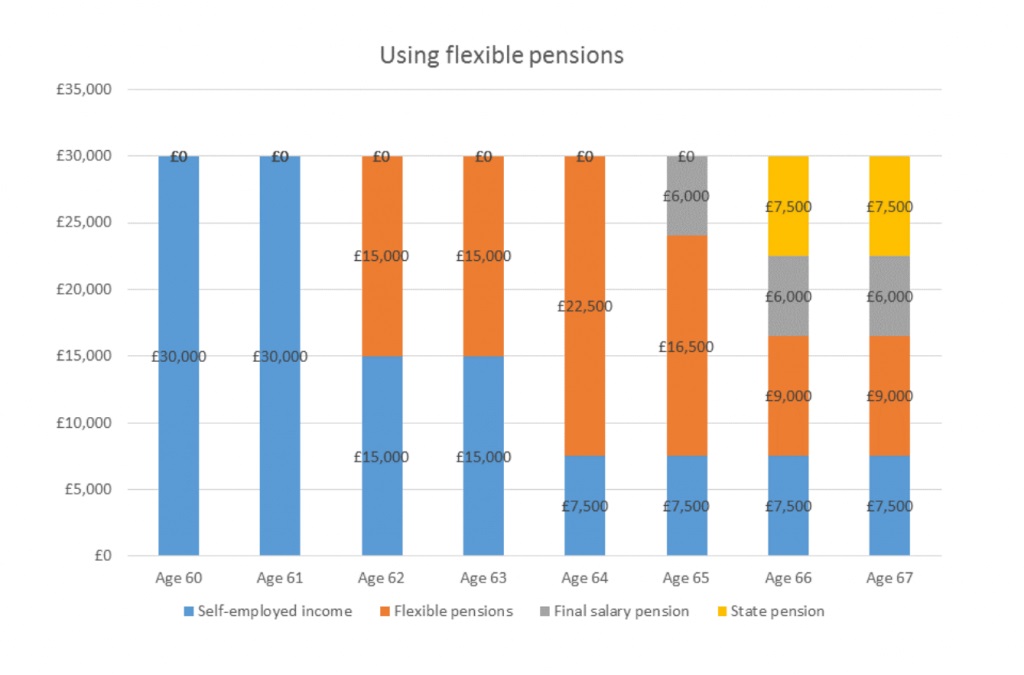

Example of working less

Anita works for a bank, which has flexible working practices. She has the same retirement plans as listed above. When she reaches age 60 she realises that her final salary pension will provide approximately 30% of her current salary. She decides that she can reduce her hours with her employer by 2 days a week, making up the difference using her final salary pension from age 60, and some other savings. Her initial plan is to see how this change works, and then possibly access her personal pension in a few years.

Taking a different job

Many people work in stressful roles. As they approach retirement they many want to take a less stressful role, or one with less responsibility. One option can be to take a part-time job. This may pay you less than your full-time employment, but you might be able to plan your retirement income around this new job.

Example of taking a new job

Anita’s role is a senior manager in the bank, which is based in London. She has commuted to work for many years, and now wants to take role closer to home. She finds a role nearer to home, which pays much less, but will mean reduced travelling to work. She knows that her final salary scheme will top up this income, and she can also plan to access her personal pension before her state pension begins at age 67. In addition, her new, lower-paid job will attract less income tax, which could be a factor in her decision.

Action:

- Consider your options for income sources in retirement. Could you take some income from non-work assets (such as pensions), reduce your hours, or change jobs?

Planning your retirement budget

When planning your retirement the obvious first step is to take a close look at how your finances will change once you stop working.

From a purely practical standpoint you need to be sure that you will have enough money to be able to fund the retirement you want. Of course, you want to be sure that you will never run out of money.

How your retirement income may change

Possibly the biggest change you may notice when planning retirement is that you will move from a stable monthly income to something different. You are likely to receive some guaranteed income, some regular income, and some variable income. This depends on the sources of your retirement income.

This change can be unsettling, as you may not feel as secure as you might have been when working. You will need to put in place a plan to ensure that your retirement income can continue no matter what happens. Financial Planning in retirement will focus on the sources of income, and their possible effects in difficult periods.

Sources of retirement income

We explore the technical details of many of these retirement income sources in the section below.

- State pension

The state pension is a guaranteed source of income in retirement. Most people in the UK will qualify for the state pension, but not necessarily the full state pension. - Company pension

If you have worked for an employer then you may have built up a company pension fund, which you could use to provide retirement income. - Defined benefits pension

Many employers provided defined benefits pensions in the past (less so today). This is a guaranteed source of future retirement income. - Personal pension

A personal pension is a way for you to save for your retirement income. This will provide you with a fund that can be converted into income in retirement. This is a type of defined contributions pension. - Retirement annuities

Retirement annuities are used to convert retirement funds into guaranteed income for life. - Flexible pensions

You can use flexible pension rules to dip into your pension funds to provide flexible income. This can be more tax-efficient, and vary to your needs as they change. - Other investments

Retirement income could come from investments such as shares, or other investment accounts. - ISAs

ISAs can be used to provide tax-free retirement income. - Property

Property may be useful in retirement to provide you with a stable income, although this does come with other complications when managing the asset. - Working

You are allowed to continue working in retirement, even if it is for a short period, or part-time. - Inheritance

You may receive an inheritance in retirement, possibly from an elderly relative. This could be used to top up your retirement income. It can be difficult to predict if you will receive an inheritance, or when it might come to you.

How will your expenses change in retirement?

When you retire your expenses are likely to change in a number of areas. You can plan this to help you to establish whether you can afford to retire.

A starting point should be to examine your existing household budget. You can examine which expenses will change, which will cease, and whether new expenses will be required. Retirement does not have to mean living on less money. However, retirees often find that they need less to live than the needed at other stages of their lives.

Retirement expenses that may increase

- Leisure

If you have more time, it is reasonable that you will spend more on leisure activities. This could be hobbies, socialising, sport, meals out etc. - Utilities

Many retirees spend more time at home than when they were working. This inevitably means higher heating bills. In the past, the cost of heating your home has risen at a rate faster than inflation. - Health

If you experience declining health in later years you may find that you have increased expenses for health-related activities – prescriptions, treatments etc.

Retirement expenses that may reduce

- Travel to work

Less travel to work can mean a significant reduction in expenses related to this activity. - Car expenses

Some retires are able to move from having 2 cars to 1 car. This saves the running costs of the second car. - Income tax

If you earn less money, you pay less income tax. Income tax is a large proportion of many workers’ expenses, especially if you are a high earner. - Housing costs

Many retirees are able to buy their home before they retire. Therefore, if you have no mortgage you can plan for no ongoing expenses in this regard. Of course, other housing costs are likely to continue – rent, maintenance, council tax etc. - Children

Most people who retire find that children are no longer living with them, so generally these associated costs tend to cease.

New retirement expenses

- Leisure

You may plan to take up new activities, or memberships. This can increase your expenses. - Holidays

If you have more time you may decide to take additional holidays, which of course can cost more money.

Action:

- Prepare 2 budgets – the first should be your income and expenses for your existing situation. The second should be your expectation of income and expenses once you make your planned retirement changes. This will help you to understand if you expect to be on track to retire when you want to.

- Think about whether your likely retirement income is guaranteed, secure, or flexible.

- Consider what expenses are necessary, such as food or utilities, versus those that are desirable such as holidays or socialising.

Avoiding disaster in retirement

You can do a lot of planning for your retirement, and you may come up with a new expenditure budget, which appears to be funded by your future sources of income. However, life tends to change over time, so it helps to take account of what could go wrong in retirement.

Of course, it is difficult to predict the future, so your assumptions will probably not be correct. Therefore, it makes sense to build in some additional buffer to cope with some of these possible retirement issues.

You should regularly review your retirement plans to make sure they are still on track.

Changing health in retirement

You may have to deal with health issues in retirement. This is a difficult area for your retirement planning, but many people are concerned about the impact of their health in later life.

We have already established that the average retirement period is longer than in the past, because we are living longer on average This is relevant, but does not answer the question of whether you will need additional medical treatment or nursing care in your retirement.

Disability-free life expectancy

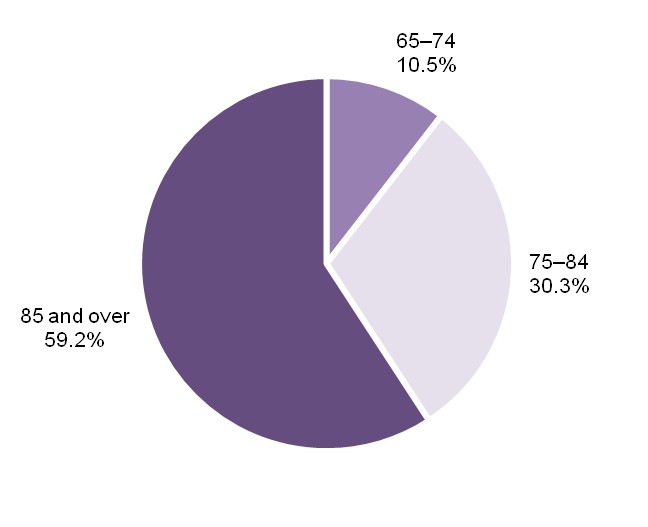

It is possible to estimate on average how long you might live in retirement before you have to deal with a disability. The latest data from the Office for National Statistics suggests that for those already aged 65:

- men can expect 10.5 years disability-free;

- women can expect 11.2 years disability-free.

This means:

- the average man in the UK can expect to be free of disability to age 75;

- the average woman in the UK can expect to be free of disability to age 76.

Of course, you are not average, so your own retirement circumstances will be individual to you.

Therefore, on average in the UK:

- Men live to age 84, and develop their first disability at age 75, meaning they live with a disability for 9 years

- Women live to age 86, and develop their first disability at age 76, meaning they live with a disability for 10 years

Clearly, it is within this period of disability that you may require nursing care in your retirement.

How likely are you to need nursing care in retirement?

The ONS estimates that, based on the 2011 census, the portion of the UK population aged over 65 grew by 11% between 2001 and 2011. Despite this, the numbers in care homes only rose by 0.3% in this period.

The study estimates that in 2011 3.2% of the over 65 population were receiving nursing care in a care home.

Breakdown of the over 65 population in care homes (ONS)

Of those in a care home, 214,000 were women, and 77,000 were men. Therefore women appear to be nearly 3 times more likely to require nursing care in a residential home than men. Most care residents are single, suggesting that having a partner enables you to put off needing to pay for nursing care.

Of course, many more people receive nursing care within their own home. The ONS estimates that 600,000 people were unpaid carers (up to 5.8% of the population aged over age 65), suggesting that care is often provided in the home first, and people move into care homes only when their needs become too acute, or they no longer have a partner able to provide nursing care.

Overall, it seems that 9% of the over 65 UK population was receiving nursing care either in their own home from a relative, or in a residential nursing home.

You can read more about nursing care here.

Planning for health changes in retirement

Given the data above, it can be difficult to plan for nursing care costs in retirement. When we produce retirement plans, we assess this situation from the worst possible position, just to test whether your retirement plans could cope. The difficulty is knowing whether you are likely to require nursing care in retirement, when it might happen, for how long, and what the cost would be. There are so many variables here that it can be difficult to plan.

The UK Government announced an improvement to the care arrangements for England and Wales in 2021. This has yet to be finalised, but the change to the regulations means that the maximum you should be expected to pay for nursing care is £84,000. Unfortunately, there is little detail on limits to the cost of food and accommodation will be limited, if at all.

- Plan for reasonable increases to health expenditure

You might make a sensible allowance for increased retirement health expenses, perhaps form age 75 onwards. This could allow for additional health-related costs such as medical prescriptions and treatments. - Plan for the worst-case scenario

The worst-case scenario might be where one partner requires nursing care in retirement, while the other has to maintain their family home. This would involve paying significant care costs, and the usual costs of running a home. If you are single the position is less severe – if you end up living in a nursing home you could sell your house to pay for care.

Action:

- Estimate the effect of deteriorating health based on your personal health history.

- Estimate the costs of future care in your home if you become less active.

- Estimate the cost of nursing care for the worst-case scenario.

Death of a partner in retirement

Unfortunately, you also need to consider the effect of death of you or your partner on your retirement plans. When a partner dies 3 major issues affect the retirement planning:

Reduced expenses

It is reasonable to assume that some expenses will continue after one partner dies. However, some expenses will change. For example, after a partner dies there will be a reduction in the budget for food and clothes.

Movement of assets

Usually, when a partner dies their will dictates how assets are distributed. This can have important effects on the surviving partner, which are sometimes positive but often negative. For example, certain assets might pass automatically to the partner. Other assets might pass to other family members.

- Property

It is common for property to be held as a joint tenancy. This means that the surviving joint owner automatically takes ownership of the portion of the deceased person’s share after their death. Sometimes a person may gift their share of a property in their will (using a tenancy in common). This might take place if your partner has children from a previous relationship. - Cash and investments

These assets typically pass according to the instructions of the deceased person’s will. You should check the provisions of their will as the survivor may have less value in assets than they might think. Special rules exist for ISAs to pass to surviving spouses. - Pension plans

Pension plans usually pass outside of the will, and this can mean that the surviving partner does not receive all the retirement benefits that their deceased partner would have received. For example, older pension plans may pay out a tax-free lump sum to the surviving partner, (if they have been nominated to receive these benefits). Newer pension plans allow for the survivor to continue with the pension plan without having to take a lump sum.

Loss or reduction of income

It is common for a surviving partner to experience lower income than they received prior to the death of their partner. This may not be an issue if expenses also reduce. However, in some cases the death of a partner can have significant implications, especially if one partner has greater retirement income than the other.

- State pension

The state pension pays to individuals, so if your partner dies, the income will usually fall – their state pension will not be paid after they die. - Pensions not in payment

Some defined benefits schemes pay death benefits that do not match the guaranteed income you would expect after retirement. Other schemes typically pay the fund to whoever you nominate. Not every scheme pays death benefits in the way you might expect. If you are not married, some defined benefits pensions may not pay anything to the surviving partner. - Pensions in payment

For guaranteed income such as defined benefits schemes, or retirement annuities, the death of the pensioner usually has an impact on their surviving partner. It is common for retirement benefits to continue after the death of a partner, but often only to a spouse; in almost every situation after the death of a partner, the income from the pension plan will reduce. You may receive reduced death benefits from a retirement annuity after the death of a partner, but only if these were built into the contract when it was set up. If you have flexible pensions, then the remaining fund is likely to pass to whoever was nominated. - Earned income

In most situations, this is likely to stop after the partner dies - Investment income

This may continue after a partner dies provided that the asset passes to the survivor.

Action:

- Prepare an outline budget for after a partner dies

- Examine the wills of both partners

- If you do not have a will consider getting one written. If you die without a will your assets may not pass to who you want them to.

- Consider which assets pass to the surviving partner, and which move elsewhere after death. You can also think ahead about options that exist in this situation.

- Assess whether who you have nominated to receive pension benefits and other assets like life assurance.

- Check the death benefits of all pension plans

- Make sure you understand the nominations made for death benefits and change these if appropriate

Running out of money in retirement

When you are planning your retirement, you should think carefully about how long your money will last, especially if you plan to use flexible pensions, or drawdown to access your capital.

Your retirement goal should be to ensure that your money lasts at least as long as you live. You can achieve this by using the concept of the Safe Withdrawal Rate. This allows you to calculate how much you can afford to withdraw from your pensions (and other retirement savings) before your capital is exhausted.

What is the Safe Withdrawal Rate in retirement?

The Safe Withdrawal Rate is the calculation of how much you can afford to spend from your retirement savings before you run out of money. This allows you to work out the amount of income that you can take, based on a variety of factors. Bear in mind that this calculation may change over time, so you need to review your progress.

Why is the Safe Withdrawal Rate important?

When you retire, you will need to generate an income to fund your expenses, especially if you are no longer working. This retirement income may come from a variety of sources:

- Pension savings

- Defined benefits pensions

- State pension

- Investments or savings

- Property

- Working income

Some of these income sources may be guaranteed, and therefore would continue regardless. The State pension or a defined benefits pension would be an example of guaranteed income.

However, if you have savings in pensions, or other accounts, then you have 2 main choices for this retirement income:

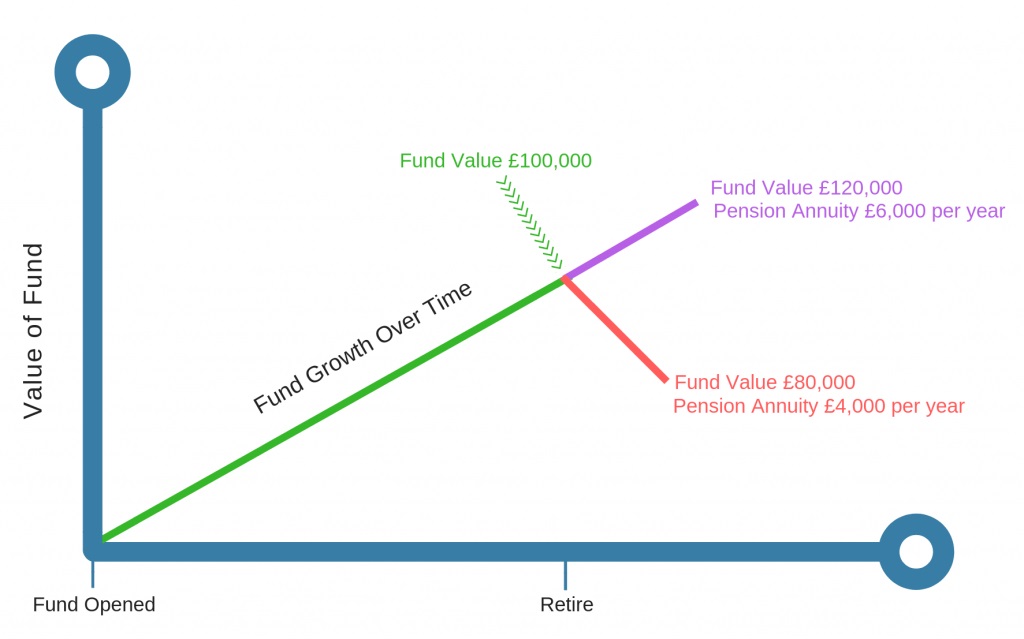

Guaranteed income

Traditionally, pension savings would be converted to a retirement annuity. This is a guaranteed income for life, and is still appropriate for many people who want certainty for all or some of their retirement income. If you want certainty with your income then this product is appropriate for you, and you would not need to use the Safe Withdrawal Rate, since the future income would not be able to be changed.

Stable income

Some income sources are relatively stable, but do not have a guarantee. This might include rental income from property. You can generally rely on this income in retirement, but occasionally a crisis will mean your income reduces or ceases.

Flexible income

It is common to use flexible pensions for retirement income, especially in the earlier years of retirement. This allows you to access your retirement savings when it suits you, and to alter the amount you take as your circumstances change. The downside is that you need to manage the income taken carefully – hence the need for the Safe Withdrawal Rate calculation.

Combining guaranteed and flexible income – an ideal retirement?

In many ways, a stable retirement can be achieved with a combination of guaranteed income and flexible income. Imagine that your standard expenses (such as food and utilities) are £25,000, and your discretionary expenses (such as holidays and leisure) are £10,000. If your guaranteed income covers the basics, then the variable income may be under less pressure as you could continue to live even if these sources of income were to reduce.

Factors that influence the Safe Withdrawal Rate

The Safe Withdrawal Rate concept requires you to make assumptions about the future that may not prove to be true. That is why you should regularly review your retirement income, based on the reality of your life, and how it is changing.

How much retirement income do you actually need?

Before you start your Safe Withdrawal Rate calculations, you should consider carefully how much retirement income you actually need. A variety of factors will influence this decision. Think about how your life will change after retirement, and what your expenses will be. Certain spending will reduce, but other areas may increase.

The amount of retirement income you need will influence your retirement withdrawal rate. The Safe Withdrawal Rate calculation will then help you to determine whether your retirement plans are likely to be secure, or more precarious. In practice, the lifestyle you lead, and your actual expenses, are much more likely to influence how much you withdraw from your retirement savings, whether this is a safe withdrawal rate or not.

Overspending in retirement

Clearly, if you take too much income your retirement savings will run out sooner than if you take less income. You will need to maintain a delicate balance between your short-term income requirements, and long-term investment growth.

The size of your retirement savings

Clearly, the larger your retirement savings, the more income you should be able to withdraw from the pot. The whole purpose of the Safe Withdrawal Rate calculation is to establish just how much you can take out.

Longevity

The length of time you expect to live is very important when calculating the Safe Withdrawal Rate in retirement. Try not to under estimate how long you expect to live, as it may be longer than you think.

Inflation in retirement

The Safe Withdrawal Rate calculation should take into account the future increases to your spending as the cost of living increases. The effect of this can be catastrophic to your spending power in retirement. Essentially, the withdrawals from your retirement savings are only likely to increase in the future, as prices increase. This will accelerate the depletion of your retirement savings if your income needs are too great.

Investment risk in retirement

In general, the more investment risk (measured by volatility) you are prepared to accept, the greater the growth you can assume on your retirement savings. Many retirees accept less volatility than may be sensible, given that they need their retirement savings to last for 30 years or more. If you are prepared to take greater risk, you can assume more growth in your Safe Withdrawal Rate calculations, and your retirement income is likely to be higher. If you want to be more cautious, then the withdrawal rate is likely to be lower.

Sometimes taking too much investment risk can introduce additional strain on your retirement income. For example, if you r retirement accounts are held in volatile investments, a short-term temporary fall in value may be significant. If this is not managed properly, the timing of these falls in value can be detrimental to your long-term retirement income.

Tax on your income

Retirement savings are likely to be taxed, although you can use pension tax-free cash to manage your income, especially in the early years of withdrawals. Take this into account when you review the Safe Withdrawal Rate against the income you actually require to live your lifestyle in retirement. You need to make sure that the Safe Withdrawal Rate is enough after tax is deducted on your income (or capital withdrawals from other investments).

Investment charges

If you plan on using flexible pensions in retirement, then the account will have charges, which will reduce the investment growth you can assume. Take this into account in your Safe Withdrawal Rate calculations.

Managing investment volatility in retirement

You should also take account of volatility in your investment portfolio. If your investments fall in value then the income you withdraw can accelerate the reduction in capital, meaning you run out of money sooner. You should have a plan in advance to cope with inevitable investment volatility

As a simple example, if you hold £100,000 in retirement savings. If we do not assume any investment growth, or any of the other factors listed above, then you could safely withdraw £10,000 per year for 10 years (without any increases for inflation). If your investment falls in value by 30% to £80,000, then the same withdrawal amount would mean you run out of capital in 8 years. The timing of any fall in value can have a significant impact on your Safe Withdrawal Rate in retirement.

Natural income

Some people manage investment volatility by taking the natural income from their retirement accounts. This means that you can allow the underlying capital to rise and fall according to market performance. The income paid by those investments determines the Safe Withdrawal Rate. If you use this method you need to have a plan in place to deal with the potential drop in income if your assets fall in value. You may need to spend less money, or use alternative capital, until the account recovers in value.

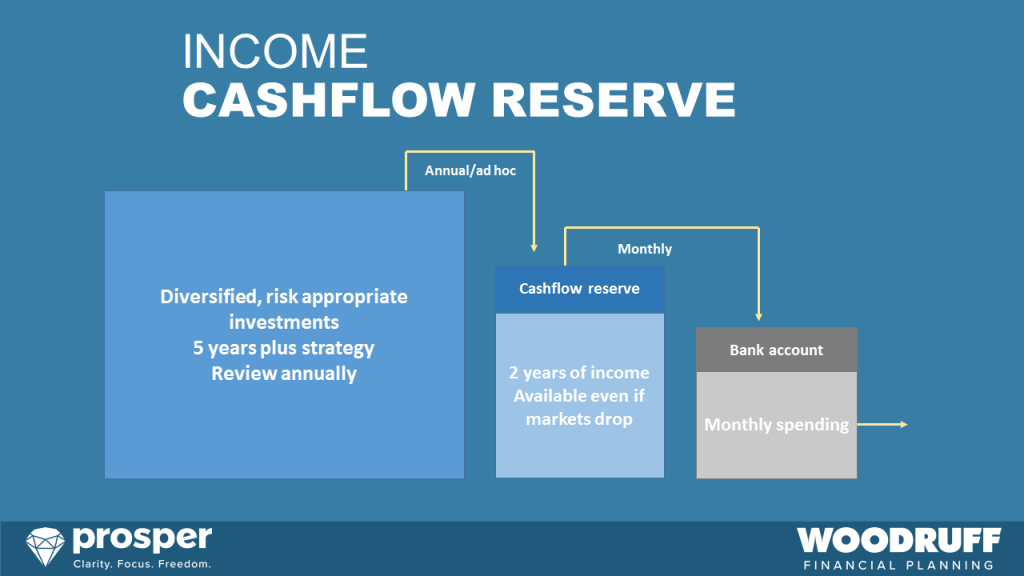

A retirement income cashflow reserve

A simple solution to investment volatility is to set up a retirement income cashflow. This is a buffer account with 2 (or more) years of variable expenses put aside.

This allows you to let your long-term retirement capital rise and fall according to normal market fluctuations. If your long-term retirement investments fall in value sharply, you can temporarily stop income payments, hoping for the capital value to recover.

The cashflow reserve account allows you to continue with your expected retirement income levels during that period. Of course, it is possible that investments could take than 2 years to recover, we use this concept as a reasonable compromise since holding too much cash will hold back expected investment growth in normal periods.

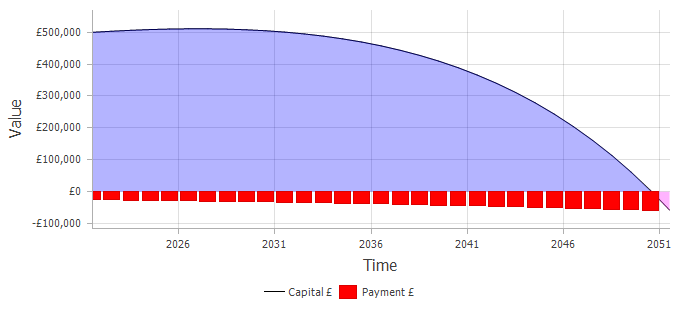

Example

Quentin holds a personal pension worth £500,000. He calculates that he can sustain £25,000 income per year for nearly 30 years, if investments grow at 6% per year, and his income grows by 3% per year.

Other factors such as withdrawal timing, variable investment growth, charges, inflation, and tax could have a significant impact on these calculations.

If Quentin’s retirement funds fell in value sharply, this could impact the length of time his retirement income might last. Imagine that Quentin’s retirement plan fell in value by 20%. If this fund never recovered, Quentin’s retirement income might last 8 years less using the same assumptions.

In the inevitable situation where Quentin’s retirement savings fall in value (this happens regularly, and should be expected), he will have to make a decision. What changes should he make to his retirement income to ensure that the capital value is not impacted too much?

Quentin could decide to reduce his income temporarily to allow his capital to recover. This is not a fun solution in retirement.

If instead, Quentin holds a cash reserve of £50,000, he knows he can allow his lifestyle to continue for 2 years before he has to make changes to the income level. We would typically expect investment markets to recover during this period, although this is not guaranteed.

The 4% rule and the Safe Withdrawal Rate

Many people use a general rule of thumb when calculating the Safe Withdrawal Rate in retirement. In 1994 a US financial planner published a study indicating that 4% was the Safe Withdrawal Rate for retirees planning to increase their income in retirement, and make their capital last for 30 years. Many additional studies have been performed since this research was published, and these generally suggest caution in using this approach, since markets are quite different in the current environment, and your investments may not match the study’s sample portfolio. The reality is that this is not a simple approach that suits every situation, and every retirement.

Action:

- Estimate the retirement income you have for guaranteed or variable sources

- Understand the difference between your standard expenses and variable expenses.

- Estimate your retirement income needs

- Understand the factors that influence your retirement income needs:

- How long will you realistically live?

- How will the cost of living rise in retirement?

- How much risk are you prepared to take in retirement?

- What tax will you pay in retirement?

Types of pension schemes

Planning your retirement can involve solving technical issues using various pension products. This section of the Planning your Retirement Guide aims to cover some of the most important types of pension schemes when planning your retirement. However, please bear in mind that this is a vast area, which is beyond even this extensive guide. This is not intended as a definitive technical guide to planning your retirement. However, the information below can help you to understand the main types of pension schemes.

The State pension

The state pension is a major source of guaranteed income for most people.

Eligibility for the state pension

You build up your state pension by paying National Insurance contributions during your working life. You need to contribute National Insurance for at least 10 years to qualify for the state pension. The maximum state pension is payable if you contribute for 35 years.

You can also qualify for state pension credits if you are unemployed, are in full time education, or are a carer.

The state pension age

The state pension age is different depending on when you were born. The table below sets out the state pension age.

| Date of birth | State pension age |

| On or before 05/04/1960 | 66 |

| 06/04/1960 to 05/03/1961 | Between 66 and 67 |

| 06/03/1961 to 05/04/1977 | 67 |

| 06/04/1977 to 05/04/1978 | Between 67 and 68 |

| 06/04/1978 or later | 68 |

The state pension age is likely to change in the future, as the population lives longer. The latest review into state pensions in March 2023 recommended that the government bring forward planned increases to the state pension age. The government announced that this will not be decided until at least 2025, but it is safe to assume that if you were born after 1970 that your state pension age might change in the future.

You can find out your state pension age here.

How much is the state pension?

The state pension currently pays a maximum of £203.85 per week, which is equivalent to £10,600.20 per year, or £883.35 per month. The state pension pays income every 4 weeks. Therefore, the full state pension would be paid as £815.40 every 4 weeks.

To qualify for the maximum state pension you must pay qualifying National Insurance contributions for 35 years. If you pay contributions for more than this, you will not get more than the maximum. Generally, you qualify for National Insurance credits if your income is greater than £123 per week. You start paying National Insurance when your earnings are greater than £242 per week. Different levels apply to self-employed workers.

If you accrue fewer years of contributions, your state pension will be reduced on a proportionate basis.

Annual increases to the state pension (the triple lock)

The state pension is particularly valuable since it increases in line with inflation each year (known as the triple lock). The government generally increase the state pension each year by the higher value of inflation (CPI), average earnings, or 2.5%. The triple lock was abandoned in 2022/23 due to the high rate of earnings growth towards the end of 2021. Instead, the state pension rose by 3.1%, which was the rate of increase in CPI at that stage. However, this was subsequently reinstated and the state pension rose by 10.1% in April 2023.

Is the state pension taxed?

The state pension is not taxed, but is taxable. This is a classic politician fudge. Essentially, your state pension will form the first tranche of your income, and therefore uses most of your income tax personal allowance. Ultimately, this means that your other income sources will be taxed at a greater level.

State pension forecast

The easiest way to find out your projected state pension is to obtain a state pension forecast. You can do this in 2 ways:

- Complete a BR19 form

You can print off a BR19 form to apply for a state pension forecast. This process takes around 2-4 weeks. - Use the Government Gateway

If you have your own Government Gateway account, you can obtain your state pension forecast within a few minutes. Click here to obtain your state pension forecast online.

What does a state pension forecast show?

Your state pension forecast shows 4 important pieces of information:

- The date and age of when you can claim the state pension”

- Your total expected state pension at retirement age

- The accumulated state pension to date

- How many more years you need to contribute to gain the maximum state pension

The state pension forecast is very useful to allow you to properly plan for your retirement income.

- Maximum state pension

If your state pension forecast shows that you have already qualified for the maximum state pension, then no further action is required. You can rely on the future income from your state pension age.

- More contributions required

Your state pension forecast may show that you need to pay further National Insurance to qualify for the full state pension. If you expect to work for these years, then you are on track, although you should regularly review your progress towards the full state pension. If you are no longer working, but have not yet contributed enough to qualify for the full state pension, you can consider topping up the state pension by making voluntary contributions.

Voluntary contributions

You may have gaps in your National Insurance contributions record. This can happen when you are out of work, have low income, or live abroad.

You can review your past National Insurance record, and can make up contributions voluntarily for up to 6 years.

Click here to check your National Insurance record online.

Once you have this data, you can easily assess whether it is worthwhile to pay voluntary National Insurance contributions.

Anita’s story

Anita came to us aged 60, and was no longer working. She obtained her state pension forecast, which revealed that she was missing 4 years of National Insurance contributions. Anita was entitled to the state pension at £160.08 per week (£8,324.16). The full state pension for 2021/22 was £179.60 per week, or £9,339.20. Therefore, with a full state pension contributions record, Anita would be able to increase the state pension by £1,015.04 per year.

Anita then obtained her National Insurance contributions record. This showed that if she were to pay a lump sum contribution of £3,054.56 then she would increase her state pension to the maximum level. Therefore, it would take Anita around 3 years to benefit from this transaction, once she claims her state pension from age 66.

How to claim the state pension

You do not receive the state pension automatically – you need to claim it. You can claim the state pension easily online.

You should receive a letter reminding you to claim the state pension within 2 months of your state pension age. You can also claim the state pension by calling 0800 7317898.

Delaying the state pension

You can delay the state pension if you do not need the income. You might delay the state pension if you receive taxable income, and want to avoid paying income tax.

You do not need to do anything to delay your state pension. If you do not claim your state pension, t will defer automatically. You can delay the state pension in chunks of 9 weeks. For each 9-week period you delay the state pension, it increases by around 1%. This works out to be around 5.8% for every year you delay taking the state pension. Of course, this will increase the future value of the state pension, which may mean that you end up paying more income tax on the increased state pension.

You can instead take the deferred state pension as a one-off taxable lump sum.

Action:

- Find out your state pension age

- Obtain your state pension forecast

- Establish if you will need further National Insurance contributions to get to the maximum state pension

Pension Plans

There are a wide variety of pension plans, and a full analysis is beyond this article. This section explores the main types of pension plans in the UK, and what the differences are. You will find information on what you need to know about your existing pension plans.

The main goal of your pension plan is to save money in a tax-efficient, long-term vehicle that is designed to provide you with a retirement income when the time comes. However, each pension plan was created to solve a different problem, and you are likely to have a variety of different schemes.

Defined Benefits Pension Schemes

A Defined Benefits pension scheme (also known as a DB scheme) is designed to provide you with a promise of a future income at retirement. These schemes typically provide you with a guaranteed income for life, which should increase in line with inflation in retirement. You do not own the Defined Benefits scheme – your employer does. You will instead be entitled to that promise of a future income based on the service with that employer.

A Defined Benefits scheme is generally less risky than a defined contribution pension scheme. However, Defined Benefits schemes are often less flexible than defined contribution pensions.

Your employer usually requires that you contribute to the pension scheme, but your employer will take the money paid in and invest it. This will be invested and used to provide the benefits at your retirement. The employer therefore owns the Defined Benefits scheme, and takes the risk that the underlying investments are enough to provide the future benefits. This requires careful management on the part of your employer, and is a weighty and expensive proposition.

Final salary vs career average

Older Defined Benefits schemes tended to be final salary pensions. This meant that your employer would provide a percentage of your final salary as an income, which would increase as your service built up over time. In extreme cases you might have built up a guaranteed income for life that was two thirds of your final salary with your employer.

Many Defined Benefits schemes have now moved to a career average basis. This is usually less generous than a final salary basis. Your employer will work out the average salary you had while employed, and will provide a guaranteed income based on the service you held with the. In most cases we tend to have a lower salary at the start of our career than at the end. Therefore a career average scheme is often intended to reduce the liability and cost to the employer.

What influences your Defined Benefits pension?

The final Defined Benefits pension usually depends on the terms of the scheme, which is set by your employer. The scheme rules will determine when you can retire, and the terms of that retirement. You will be required to make a regular contribution, but the only other factor is the length of your service with that employer.

Some schemes allow you to make additional voluntary contributions to top up your Defined Benefits scheme.

Action:

- Make a list of your defined benefits pensions

- Obtain projections from the scheme administrator to determine how much income you will get when you retire

Defined Contribution Pension Schemes

A defined contribution pension scheme (also known as a DC scheme) works very differently to a Defined Benefits scheme. A defined contribution scheme is designed to build up a pot of money in a tax-efficient long-term savings plan. This money is invested, and you hope this should grow over time. The money will be used at retirement to convert to an income, in a variety of methods.

Defined contribution pensions shift the risk to you personally. However, defined contribution schemes usually come with much more flexibility over the way you take your income in retirement.

Types of defined contribution pensions

There are many types of defined contribution pension plans. They can be divided into 2 camps: company pensions and personal pensions.

Company pensions

Company pensions can be different types of pension schemes. They are typically set up on a group basis so that your employer runs the scheme. This has a number of benefits:

- Lower cost as the scheme provides better terms based on the size of the scheme

- Easier administration as your employer handles this

- Employer contributions – this is a kind of deferred salary

However, company pensions can have some disadvantages:

- Less flexibility – perhaps the scheme will not have all retirement income options

- Less investment choice – often lower cost comes with some simplicity, which might not suit you

Examples of company pensions are:

- Auto-enrolment pensions (such as Master trust schemes)

- Group personal pensions (GPPs)

- Contracted in money purchase plans (CIMPs)

- Executive pension plans (EPPs)

- Small Self-administered Schemes (SSASs)

Personal pensions

There are a variety of personal pensions, each with their own characteristics. Personal pensions are designed for you to control your retirement saving, although your employer can still pay in to the scheme.

The main benefits of personal pensions are:

- More control over how you invest you money and take benefits

- Greater choice over how and when to generate retirement income

- Better tax efficiency of income in retirement or on death

- Potentially greater investment choice

Personal pensions can have some downsides:

- Higher costs than bigger company schemes

- Greater administration as you have to handle this yourself

Examples of personal pensions are:

- Personal pensions (PPs)

- Self-invested personal pensions (SIPPs)

- Stakeholder pension schemes (SHPs)

What influences your defined contribution pension?

The final defined contribution pension you get depends on the following factors:

- The amount you pay in

- The investment growth

- How and when you take your income

- The charges of the pension scheme

- Inflation

- Tax

Action:

- Make a list of all your defined contribution pensions

- Obtain projections from each product to establish how much income you could expect at retirement (this could change depending on the income options you change)

Tracing Old Pension Schemes

During your lifetime it is common to join a number of pension schemes. You may lose touch with a former employer, or an older scheme. IN addition, some employers cease trading, and some pension companies are acquired by other firms. Therefore, unless you are careful to keep track, you may lose sight of old pension schemes.

The good news is that you can trace old pension schemes via a Government service. All you need is the name of the pension provider, or your former employer, plus your personal details.

Click here to start tracing your old pension schemes.

Action:

- Go to the website listed above to trace any old pension schemes you may have lost contact with

Pension scheme contributions

This section of this Planning your Retirement Guide sets out the main rules and complications relating to pension scheme contributions. There are a lot of rules that govern pension scheme contributions. You need to be particularly careful if you want to make contributions that are greater than the standard Annual Allowance for pensions.

Contributions to a Pension Plan

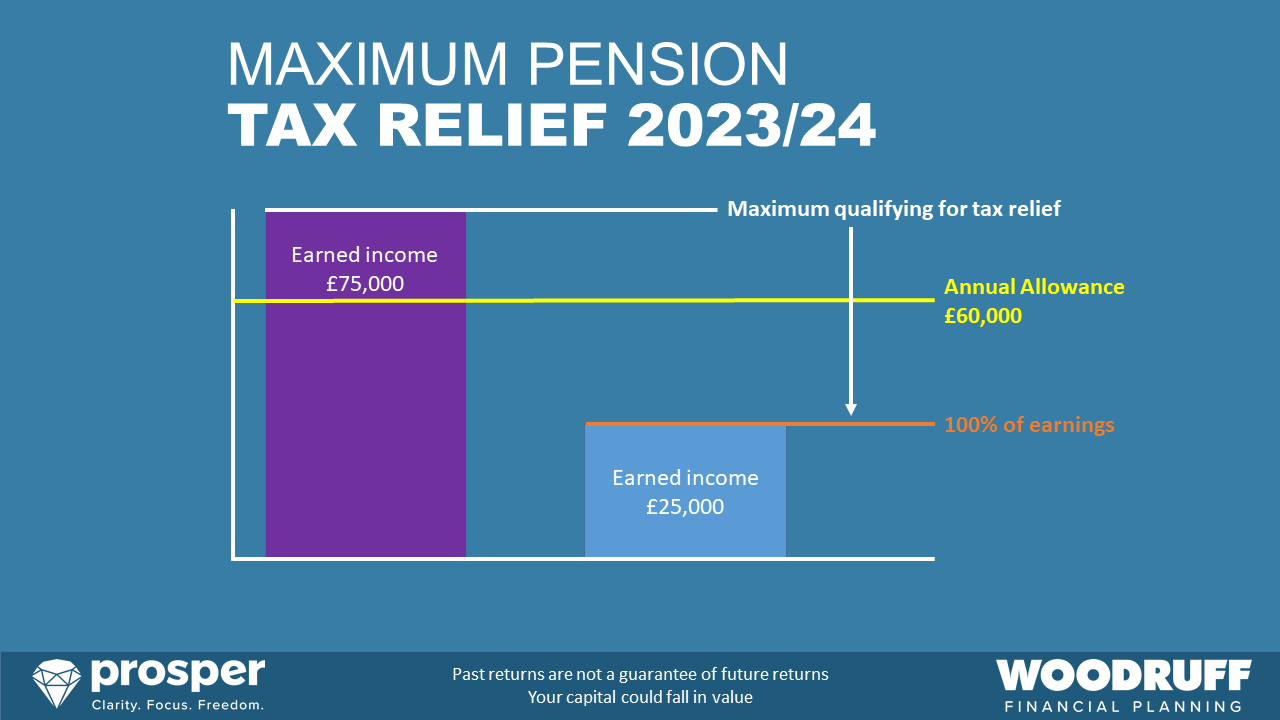

To create an income in retirement, the most likely source of contributions is from you or your employer. Importantly, the amount you can pay into a pension plan personally, and still claim tax relief, is limited to 100% of your earned income for that tax year (or £3,600 without earnings). Thus, you can only pay limited amounts into a pension plan if your income is from other sources such as rental income.

Payments to Defined Benefits schemes

For a Defined Benefits scheme your employer will set the amount you must pay to be a member of the scheme. This is usually expressed as a percentage of your salary.

Payments to Defined Contribution schemes

You can pay money into your scheme personally, and your employer or other third parties can also make payments.

Personal contributions

There are 2 methods to make personal contributions. The defined contribution pension will determine the method used.

For some schemes you will benefit from tax relief immediately – the contributions are deducted before tax is taken from your income. This means you avoid the income tax you would have paid had you not made the payment into your pension plan.

Other schemes will deduct your contributions after tax has been taken out. This means your scheme will add tax relief to the pension. You may need to take further action if you pay income tax at 40% or 45%.

Pension tax relief at source

Most personal pensions work using the tax relief at source method.

You receive your normal income, and pay income tax and National Insurance on this. From your net pay you make pension contributions. The pension scheme then applies for tax relief on the basic rate element. Under the tax relief at source method you pay pension contributions after you have paid tax, and then reclaim tax relief at source.

Pension tax relief for a 20% taxpayer

Pension tax relief acts by boosting the payments you make to your pension plan. For every £100 you pay into your pension plan, you get £25 as tax relief.

This represents a return of the basic rate income tax paid by you at 20%. So, the more you pay in, the greater the pension tax relief you can get.

Pension tax relief is one of the biggest advantages of pension plans – after all there are not many investments where you can guarantee a 25% growth on your contributions on day 1.

Reclaiming additional tax relief for 40% or 45% income taxpayers

Under the tax relief at source method, if you pay into a personal pension and also pay income tax at 40% or 45% you can reclaim additional tax pension tax relief through your tax return. Alternatively, you may be able to ask the tax office to adjust your tax code to reflect the pension plan contributions, and thus save tax at source.

- As a 40% income taxpayer your £100 contribution would attract a further £41.66 back in tax saved;

- As a 45% income taxpayer your £100 contribution would attract a further £56.81 back in tax saved.

You must remember to claim the additional tax relief due to you – it does not happen automatically. You may be able to ask for unclaimed tax relief for up to 4 years from the end of the tax year for which it is due.

Pension Net Pay method

The net pay method is used by some Defined Contribution pension schemes. This is different to the tax relief at source method.

Under the net pay method, your employer will deduct your personal contributions before applying income tax and National Insurance. This means that the net pay method deductions for your pension plan come out of your gross pay before tax. Effectively, this reduces your taxable pay, and therefore reduces the income tax as well. The contributions do not attract tax relief, but instead reduce the tax you pay. This is more convenient for 40% or 45% income taxpayers, as it means that you do not have to reclaim tax relief due to you via your tax return.

The net pay method is poor value for those who do not pay income tax. Non-taxpayers do not benefit from a reduction in tax under the net pay method. If the same workers were to use the tax relief at source method, they would get tax relief at source of 20%, boosting their pension contributions.

Net pay method boost for low earners from April 2026

Under the current rules, if a person receives a low income, they may be disadvantaged by making pension contributions using the net pay method. This is because, if that person earns too little to pay income tax (currently less than £12,570) any pension contributions will not reduce their tax. A low earner making pension contributions is likely to be better off making payments to their scheme using the pension tax relief at source method.

The new plan from April 2026 is to allow contributions to net pay pensions for low earners to receive tax relief in the same way as if these are made at source. The Government has announced legislation to equalise the tax arrangements for low earners who use the net pay method. The expectation is that these workers will receive a top up to their pension contributions from 2026.

Pension tax relief for the self-employed

If you are self-employed, you will need to account for your pension contributions in your tax return. If you pay income tax at a higher rate than 20% you will also get to reclaim the additional tax relief due.

Employer pension contributions

Your employer or other third parties can pay contributions into your pension scheme. You do not get tax relief on this money, but your employer can save some tax.

You should consider this method if you are a business owner – see below.

Pension contributions for non-earners

You can make limited pension contributions even if you are a non-earner. This applies if your income comes from other sources such as rent or investments. The only personal pension contributions permitted which attract tax relief apply to earned income.

The maximum you can pay per tax year into a defined contribution scheme from other sources is £3,600, including tax relief. This means that you will pay £2,880 as a personal contribution. £720 of tax relief is then added, making a total of £3,600 paid into the pension plan.

Many non-earners, looking for tax-efficiency, use this method. You can pay pension contributions in these situations:

- For children or grandchildren

- For your spouse

- To divert taxable savings into a tax-free pension

- To avoid inheritance tax, even after you stop working

Pension contributions for overseas workers

If you become non-resident, but previously had earnings in the UK you can still pay into a pension scheme for up to 5 years after the tax year in which you leave UK residency. In practice schemes tend to limit this to £3,600 per tax year. Therefore, if you take a job overseas you could consider continuing payments of up to £2,880 per tax year for 5 years, which would attract tax relief of £720 per year.

Pension contributions after age 75

Technically, you can pay into a pension scheme after age 75, but you will not receive tax relief if you do pay into your scheme.

Action:

- Are you making the most of the pension tax relief available to you

- Are you saving enough?

- If you are a higher rate taxpayer, are you reclaiming the additional tax relief?

The Annual Allowance for pensions

The Annual Allowance is the amount you are allowed to pay into your pension plans in any tax year without incurring additional tax.

- If your contributions are less than the Annual Allowance there is no tax to pay.

- If your pension contributions exceed the Annual Allowance, you may have to pay a tax charge. This is known as the Annual Allowance Tax Charge.

The standard Annual Allowance increased to £60,000 from 6th April 2023 (it was £40,000 previously).

When can the Annual Allowance reduce from £60,000?

The Annual Allowance reduces if the following applies to you:

- You are a high earner (total remuneration greater than £260,000); or

- You have accessed your defined contributions pensions flexibly.

Exemptions from the Annual Allowance

You do not have to test pension contributions against the Annual Allowance in these situations:

- Death of a member

- Serious ill health (meaning life expectancy is under 1 year)

- Severe ill health (meaning you are unlikely to ever return to work)

What contributions affect the Annual Allowance?

The Annual Allowance is affected by any of the following

- Contributions to your defined contribution scheme in the tax year

This could be personal payments, tax relief, employer contributions, or any other third party. - Any increase to your Defined Benefits scheme in the tax year

The Money Purchase Annual Allowance (MPAA)

Your standard Annual Allowance will reduce to £10,000 if you access your pension benefits flexibly. This is known as the Money Purchase Annual Allowance. The Money Purchase Annual Allowance increased from the previous level of £4,000 after 6th April 2023.

You will not be subject to the Money Purchase Annual Allowance if you take any of the following benefits:

- Defined Benefits scheme pension

- Tax-free cash (pension commencement lump sum)

- Defined contribution pension annuity (unless this comes from flexible benefits like a drawdown plan)

Therefore, if you take flexible income from a drawdown pension plan, the Money Purchase Annual Allowance will apply to you.

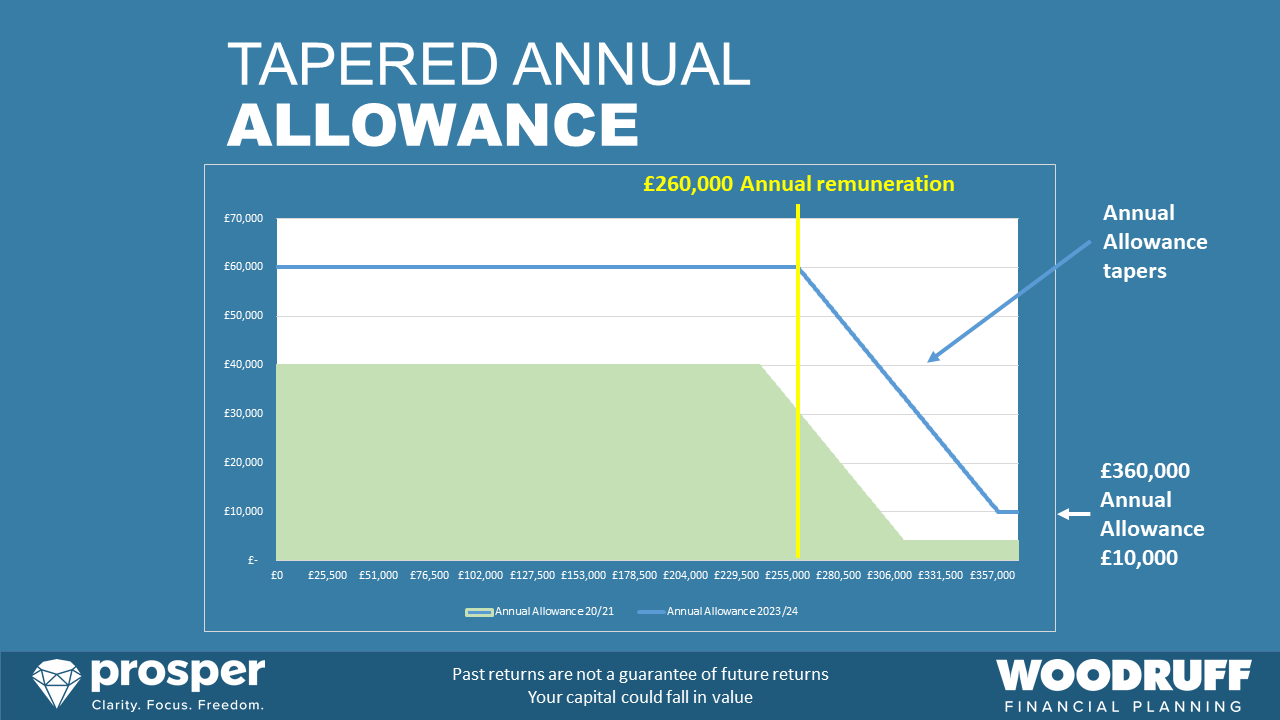

The Tapered Annual Allowance

The pension tapered annual allowance is a serious issue if you earn a high income. It could lead to significant extra tax bills.

If your total income is greater than £260,000, and you pay into a pension plan, you need to be aware of the pension tapered annual allowance for high earners. You may find that your ability to make pension contributions reduces by up to £50,000, to a maximum contribution limit of £10,000. Contributions over this tapered annual allowance attract additional tax at up to 45%. Different taper triggers apply for past years, so you need to take care if you are a high earner as the tapered annual allowance could apply in some tax years but not others.

The pension tapered annual allowance for high earners

Everyone has a standard annual allowance, which permits you to pay up to £60,000 into your pension schemes. This applies to contributions or increases to pension benefits from all sources, per tax year.

Any payments over this figure are subject to an additional tax charge at your marginal rate of income tax – 20%, 40% or 45%, depending on your earnings.

The annual allowance has reduced dramatically in recent years, from £255,000 in 2011/12 to its current level of £60,000. If you are taking taxable income using flexible drawdown then your annual allowance is reduced to £10,000 (known as the Money Purchase Annual Allowance).

If your ‘adjusted income’ is over £260,000 you may find that your ability to make pension contributions has been reduced. It is quite possible that your current pension contributions would incur additional tax at 45%.

Adjusted income over £260,000 will reduce your pension annual allowance by £1 for every £2 of income above this figure. The annual allowance for pensions will reduce to a minimum of £10,000 per tax year if you earn more than £360,000.

Prior to 6th April 2023, the tapered annual allowance started at a lower level (£240,000) and reduced gradually to £4,000 for income over £312,000. Now, the tapered annual allowance starts at a higher threshold, and reduces to a minimum of £10,000.

Prior to 6th April 2020, the tapered annual allowance started at a lower level (£150,000) and reduced gradually to £10,000 for income over £210,000.

How the tapered annual allowance makes pension planning difficult

Each tax year will be treated differently, so your earnings in one year might mean you have a reduced Tapered Annual Allowance; in other years you might have the full standard annual allowance. This can make it difficult to plan for high earners. Many high earners receive unpredictable income, such as bonuses or share awards. This additional income usually comes at the end of the tax year. Ultimately, this may mean that you are subject to the tapered annual allowance in one tax year, but not another. You may not know the full picture until you are awarded your final bonus. This will make it difficult for you to plan your pension contributions using bonus sacrifice, which is a tax-efficient method of giving up some of your bonus in exchange for tax relief into your pension.

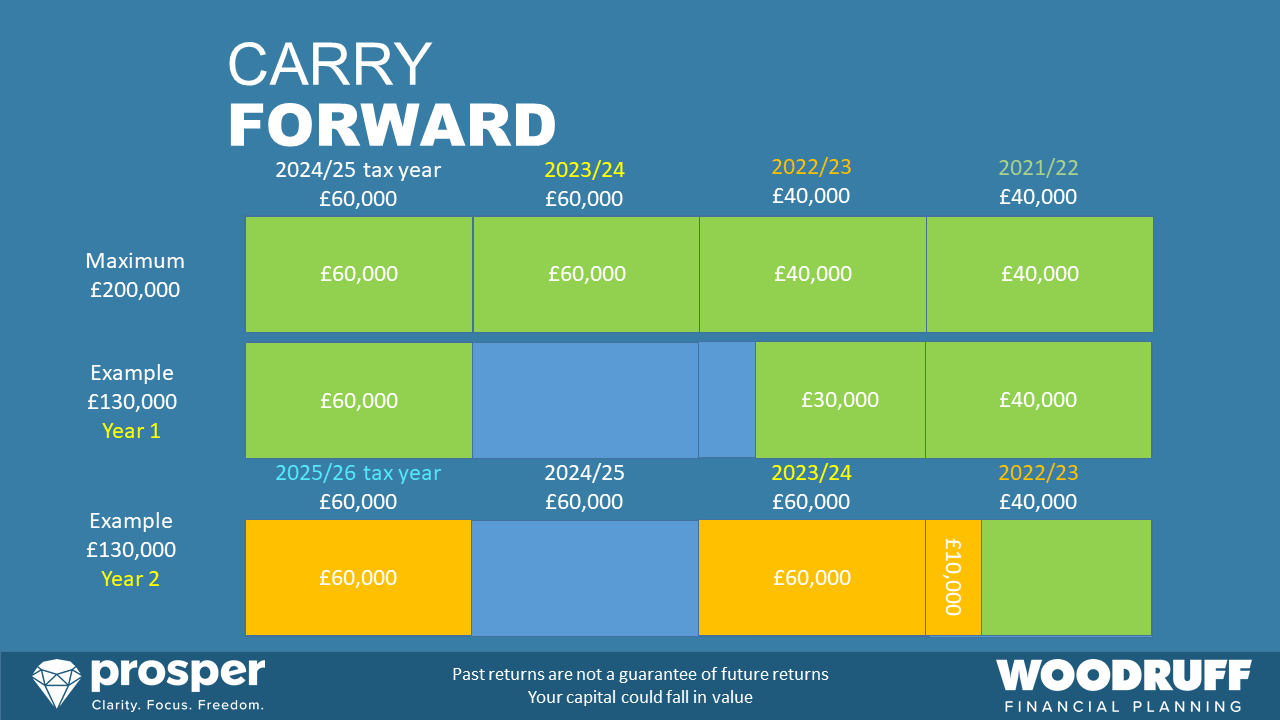

How the tapered annual allowance changed from 6th April 2023

This chart shows the effect of the changes between the 2022/23 and 2023/24 tax years. The green line shows the tapered annual allowance and how it operates from 6th April 2023, depending on your adjusted income. The blue shaded area shows the previous adjusted income bands from which applied until 5th April 2023. You can clearly see the improved tapered annual allowance. The lowest that the Tapered Annual Allowance falls to is £10,000.

What is adjusted income?

If your adjusted income is greater than £260,000 you will start to lose your annual allowance. This was £240,000 prior to 6th April 2023.

- Adjusted income includes the total of the following:

- Employment income – salary, bonus, benefits in kind

- Profits from self-employment

- Pension income

- Property income

- Dividends

- Savings income

- Taxable lump sum death benefits

- Employer pension contributions

- Salary exchange contributions

- Individual pension contributions under a ‘net pay’ scheme – usually from an occupational pension scheme or retirement annuity contract

If you pay into a personal pension, then your individual pension contributions usually come out of net pay, and therefore do not need to be added back to adjusted income.

Employer pension contributions do count in adjusted income.

Any pension contributions which may be made to reduce your taxable income, such as salary exchange, are now taken into account when determining your adjusted income for your pension annual allowance if you are a high earner.

You can use some allowances to reduce adjusted income, such as gifts to charities.

An exception – threshold income below £200,000

If your ‘threshold income’ is not greater than £200,000 in a tax year, the annual allowance is not tapered for that tax year, even if your adjusted income is over the limit. These rules are designed to protect lower earners. The Threshold Income limit was set at £110,000 prior to 6th April 2020 but did not change when the adjusted income limit was raised after 6th April 2023.

What is threshold income?

If your threshold income is less than £200,000 (£110,000 prior to 6th April 2020) then you cannot be subject to the tapered annual allowance, even if your adjusted income is greater than £260,000 (£240,000 prior to 6th April 2023). You can see that this is complex and requires careful planning.

Threshold income includes:

- Income from employment- salary, bonus, benefits in kind

- Profits from self-employment

- Pension income

- Property income

- Dividends

- Savings income

- Taxable lump sum death benefits

- Salary exchange contributions to pensions since 9th July 2015

- Individual pension contributions under a ‘net pay’ scheme – usually from an occupational pension scheme or retirement annuity contract

Importantly, this definition does not include employer pension contributions. If a salary exchange arrangement was set up before 9th July 2015 this amount is not included in your threshold income. Therefore, business owners can legitimately pay employer pension contributions to reduce their threshold income, subject to anti-avoidance measures (see below).

Example 1 – Adjusted income over £260,000

Julie receives the following income and pension benefits.

Salary of £250,000.

Employer personal pension contributions of 10% of salary per year, or £25,000.